DEEP DIVE: Online Grocery Series: The US – Market Set To Boom As Basket Sizes Grow

KEY POINTS

This is the second in our series of reports analyzing online grocery markets around the world.

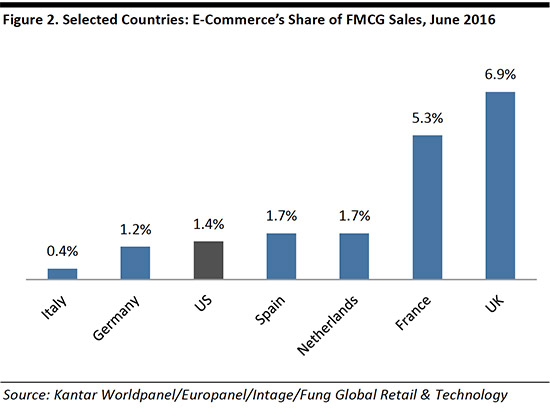

- Just 1.4% of all US sales of fast-moving consumer goods (FMCGs) were made online in June 2016, according to market-measurement service Kantar Worldpanel. This is well below e-commerce’s share of such sales in the UK and France, and barely above its share in discounter-dominated Germany. The US figure belies substantial consumer participation, however, some 31% of US grocery shoppers bought groceries online in 2015, according to research firm Mintel.

- We see two reasons for the mismatch between e-commerce’s low share of grocery sales and the high consumer participation rate. First, US online grocery shoppers are buying specific items rather than undertaking large shops on the Internet, which depresses average basket sizes. Second, these shoppers are buying groceries on the Internet only infrequently.

- We think the US online grocery market is on the cusp of a boom: major retailers such as Walmart and Kroger are piling in, and they will drive up average online basket sizes by focusing on their customers’ main grocery shops rather than on small-basket, occasional purchases. We see this acceleration happening in 2016 and into 2017 as the offerings from retailers change how shoppers use the online channel.

EXECUTIVE SUMMARY

The US is a nascent market for online grocery retailing, even though a large number of consumers are already buying groceries online.

- Just 1.4% of all US sales of FMCGs were made online in June 2016, according to Kantar Worldpanel.

- Some 31% of US grocery shoppers bought groceries online in 2015, according to Mintel.

- As of September 2016, some 7% of US consumers had bought groceries via a desktop or laptop in the past 30 days, according to a survey by Prosper Insights & Analytics, while a further 3% had bought groceries via mobile devices.

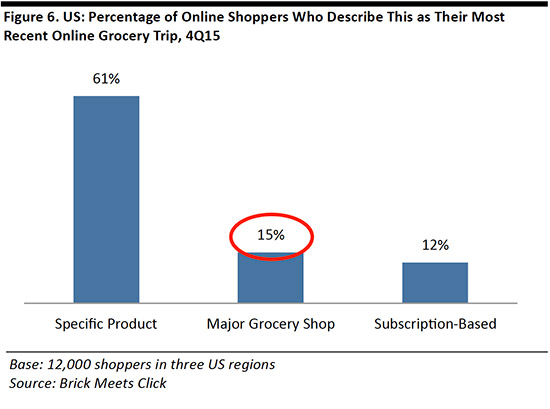

However, US consumers are mostly buying specific grocery items online, and those on an occasional basis. Most online grocery shoppers are not using the channel for their regular, big-basket shopping trips. Just 15% of online grocery shopping purchases are regular, big-basket shops, according to grocery research firm Brick Meets Click.

In the US, Amazon is the most popular online retailer for groceries, according to a number of surveys. But its most-used service is Amazon Prime, not its full-service AmazonFresh grocery offering, according to a Cowen and Company survey. For Prime purchases, Amazon sends items through the regular mail, often one at a time, making the service unsuitable for a conventional grocery shop. This further underlines that small-basket shopping is currently dominating US online grocery retailing.

Amazon’s popularity is in part due to major store-based retailers’ slowness in moving online. Walmart, Kroger and Publix are still in the ramp-up stage in terms of e-commerce and, unlike Amazon Prime, these retailers are predicated on serving demand for big-basket shopping trips.

Also, these grocery retailers are focusing on more cost-effective means than home delivery, such as at-store collection (Walmart and Kroger) and the use of third-party services such as Instacart (Publix). These US retailers appear to be striking a balance between capturing online growth and maintaining profitability.

US online grocery retail looks set to boom as average basket sizes get pushed up by the offerings of conventional grocers such as Walmart and Kroger. Given already-substantial consumer participation rates, there look to be opportunities to convert the large body of occasional, small-basket online shoppers into shoppers who conduct their main grocery shops online.

As the pace of growth accelerates, we expect e-commerce’s share of US FMCG sales to jump to around 2% or more in 2017.

INTRODUCTION

This is the second report in our Online Grocery series. Our first report looked at the UK, which is the most mature online grocery market among Western economies. The US, by contrast, is one of the least mature markets, with major store-based players such as Walmart only now wholeheartedly pushing into grocery e-commerce.

The following sections of this report will look at:

- The current and forecast scale of online grocery retailing in the US.

- How US consumers shop for groceries online, emphasizing that they tend to buy only a few items, irregularly, rather than make large-basket purchases on the Internet.

- How Amazon has a leading position, by number of shoppers, and what this tells us about grocery e-commerce in the US.

- Recent activity from major brick-and-mortar chains and the scale of their online sales in dollar terms.

- How these chains are adopting less-margin-erosive e-commerce fulfillment operations than their peers are in some more mature markets such as the UK

THE US: AN IMMATURE E-GROCERY MARKET WITH GREAT POTENTIAL

The US grocery market is worth $1.2 trillion, but only a very small share of that total is being spent online.

- In the US, just 1.4% of all sales of FMCGs were made online in June 2016, according to Kantar Worldpanel. Yet that figure represents a near doubling of share in just two years.

- That is equivalent to around $17 billion in annual online sales, we estimate.

In recent years, e-commerce’s share of US grocery sales has grown by around 0.3 percentage points per year, Kantar’s data imply. However, we expect the pace to accelerate in 2016 and 2017 as major store-based retailers pile into the online channel.

We therefore estimate that e-commerce’s share of FMCG sales will jump to around 2% or more in 2017. Kantar estimates that 6% of US FMCG sales will be generated online in 2025.

Kantar’s data effectively capture only packaged products, so categories such as fresh produce are not included in these figures. We think consumers are less likely to buy fresh categories online than they are packaged, branded goods, as most people prefer to check for quality and freshness when buying fresh foods. We therefore expect the online channel’s share of total grocery sales to be slightly below the level recorded by Kantar.

Lagging Comparable Markets

Online grocery tends to take a bigger share in countries where consumers prefer to shop in large grocery stores because it offers a better fit with large store-based grocers’ propositions and consumers’ expectations—both of which tend to center on big-basket shopping trips and the convenience of added services.

The US, however, is an exception to this. The share of FMCG sales taken by e-commerce in the US is barely ahead of that seen in Germany, a country where grocery is dominated by no-frills discounters and other smaller-store formats.

We see major US grocery retailers’ reticence to offer a full online service as a major barrier to e-commerce penetration in the US. That barrier, however, is now being lifted as major chains push online, as we will discuss later.

Other hindrances to grocery e-commerce in the US include a more dispersed population, which makes home delivery much less cost effective, and a fragmented grocery landscape characterized by regional chains.

Drilling Down to Food and Drink

Our second data set, charted below, is for food and drink only. These data confirm the tiny proportion of total grocery sales that are made online.

- American shoppers spent some $7.6 billion on online food and drink purchases in 2015, according to Euromonitor International.

- This equated to 0.9% of the total $916.5 billion spent on at-home food and drink recorded by the US Bureau of Economic Analysis.

- Euromonitor expects online food and drink sales to grow by 9.9% per year on average between 2015 and 2020.

- We think this forecast could well prove conservative. Because of the ongoing ramp-up of online grocery shopping services from major retailers, and because these retailers are likely to push up average basket sizes considerably, we think the online channel is set to grow very rapidly in the US.

HOW AMERICANS SHOP ONLINE FOR GROCERIES

A very large number of Americans are already buying groceries online—despite the online channel’s tiny contribution to sector sales. In 2015, approximately one-third of US grocery shoppers bought online, and shopper numbers jumped by about 63% year over year, according to Mintel. Unsurprisingly, Mintel noted that millennials tend to show higher e-grocery participation levels than the average population.

Data for September 2016 from our research partner Prosper Insights & Analytics showed that 7% of US consumers had bought groceries online via a desktop/laptop in the past 30 days, and that 3% had bought them via a smartphone or tablet, versus 90% having bought groceries in-store over the period.

Why Are Online Sales So Low?

Given substantial shopper numbers, why are online grocery sales so low? We identify two factors that account for the small share of grocery sales taken by e-commerce in the US:

- US online shoppers mainly buy specific grocery products on the Internet; online, they tend not to perform large-basket shops of the kind they do in stores.

- US shoppers buy grocery products online only infrequently compared with shoppers in other countries.

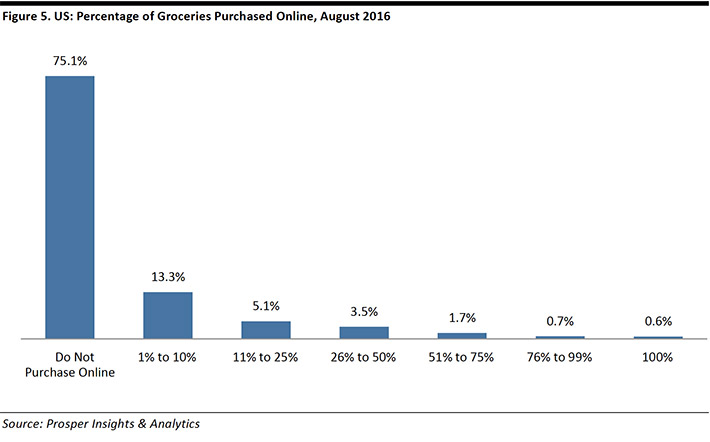

As a result, the online channel’s share of total grocery spend is very low—even among those who do buy groceries online. In the US, the majority of online shoppers do just 1%–10% of their total grocery shopping online, and an exceptionally small proportion of consumers do most of their grocery shopping online, according to Prosper.

For comparison, a Mintel UK survey in December 2015 found that 11% of British Internet users do all their grocery shopping online and a further 12% do most of their grocery shopping online.

Big-Basket Shoppers Account for a Minority of Online Shoppers

A large majority of those who say they are shopping for groceries online are actually shopping only for specific products. Just 15% of online grocery shoppers are doing a main grocery shop on the Internet, according to Brick Meets Click.

We think this is very important to understanding the discrepancy between the sizable number of Americans saying they buy groceries online and the tiny contribution the channel makes to category sales. Those looking for specific products may be purchasing just one or two niche products or may be buying very occasionally as gift purchases.

In turn, this suggests to us that there are major opportunities for retailers to push up channel sales by converting existing online grocery shoppers to main-shop shoppers.

US Online Shoppers Buy Only Infrequently

Compounding the lack of scale in the channel is the fact that many shoppers who buy groceries online do so only infrequently. We think this is linked to the abovementioned specific-product focus of most online grocery shopping.

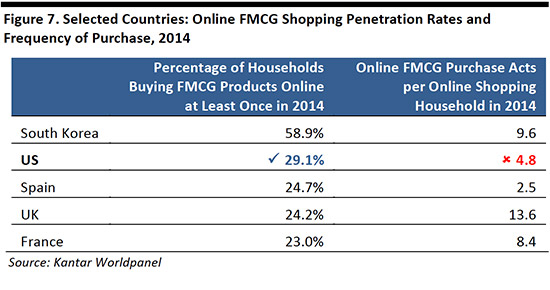

The data in the table below are from 2014, but we think the relative performance in the countries shown is unlikely to have changed substantially since then. Mature e-commerce markets such as the UK, France and South Korea are marked by their higher frequency of purchase versus the US. The data show that the hindrance to greater online sales is infrequency of purchasing rather than penetration levels—because a greater proportion of households bought online in the US than did in France or the UK, for instance.

AMAZON DOMINATES US ONLINE GROCERY

In mature markets, brick-and-mortar grocery stores hold leading positions in grocery e-commerce: we see this trend in the UK and France. In the nascent US market, however, Amazon holds a dominant share—at least by number of shoppers or shopping trips.

- Amazon attracts 48% of all online grocery shopping trips, according to a fourth-quarter 2015 Brick Meets Click survey of 12,000 consumers in three US regions.

- Some 38% of US shoppers who buy groceries online do so at Amazon, according to a Morgan Stanley survey also undertaken in the fourth quarter of 2015. The percentage figure was down marginally from

39% in the first quarter of 2015. - In a survey of 2,500 US consumers in February and March 2016, Cowen and Company found that 49% of online food and beverage shoppers used Amazon Prime (which offers expedited shipping by mail), while 18% used AmazonFresh (which is Amazon’s full-service grocery service that uses its own delivery trucks) and 11% used Amazon Prime Now (which is Amazon’s rapid-delivery service that uses couriers).

We think this last data set from Cowen is perhaps the most telling because it uncovers the split in usage of Amazon’s different grocery services:

- Only a minority of Amazon’s grocery customers are using the full-service AmazonFresh, which is set up for big-basket shopping.

- A much greater proportion of shoppers are using Amazon Prime, which delivers groceries the same way electronics, apparel and other nonfood items are delivered—through the mail and often in separate packages (this depends on the dispatch options chosen). This kind of fulfillment is not set up for conventional big-basket shopping trips.

This AmazonFresh/Amazon Prime split supports the findings noted above, that the majority of US online grocery shoppers are buying specific products when they shop online rather than doing their regular, big-basket grocery shopping.

However, we expect Amazon to push AmazonFresh in response to the roll-out of online grocery services from major chains such as Walmart and Kroger. In October 2016, Amazon cut the fee charged to customers for its AmazonFresh and it was reported that the chain could introduce curbside pick-up services. We also see opportunities for Amazon to introduce the delivery model that it uses in the UK—using third-party courier firms rather than its own fleet of delivery trucks.

Lastly, we note an apparent worldwide correlation between high levels of usage of Amazon for grocery shopping and undeveloped e-grocery markets:

- Morgan Stanley’s fourth-quarter 2015 survey found that in immature e-grocery markets, Amazon captures the highest share of online grocery shoppers among the countries surveyed: in India, Amazon accounted for 54% of online grocery shoppers, while the figure was 40% in Germany and 38% in the US.

- Mature e-grocery markets see Amazon capture a relatively lower share of shoppers: the survey figures were 15% in the UK and 14% in France.

These figures further underline that Amazon is principally a retailer used for irregular or small-basket grocery purchases.

After Amazon, Walmart is the most popular online grocery retailer in the US. According to Cowen, 30% of online food and beverage shoppers buy from Walmart.com; according to Morgan Stanley, some 38% of online grocery shoppers shop the site. We expect average grocery shopping basket sizes to be substantially higher at Walmart than at Amazon.

- We estimate that, in 2015, Amazon’s North American gross merchandise volume was around $97 billion; this is the value of all goods sold, whether sold by Amazon or by third-party merchants. If we make a ballpark estimate that 2%–3% of these total sales were in grocery categories, it suggests that Amazon North America’s grocery sales totaled approximately $2–$3 billion last year.

BRICK-AND-MORTAR PLAYERS FINALLY PILE IN

Amazon enjoys its lead in shopper numbers largely because top US brick-and-mortar grocery chains have been laggardly in venturing online. Walmart and Kroger have pushed into e-grocery only in the past couple of years, and they have been doing so primarily through at-store pickup services rather than through home delivery.

Walmart: Now Offering Pickup at Nearly 400 Locations

Offline market leader Walmart rolled out its Pickup at-store collection service across 2014. The company began extending its Pickup service to new markets and expanding it in existing markets beginning in April 2016. At the end of Walmart’s fiscal second quarter 2017 (latest), the company was offering pickup in 60 markets and at nearly 400 locations, up from 150 locations two quarters earlier.

Offline market leader Walmart rolled out its Pickup at-store collection service across 2014. The company began extending its Pickup service to new markets and expanding it in existing markets beginning in April 2016. At the end of Walmart’s fiscal second quarter 2017 (latest), the company was offering pickup in 60 markets and at nearly 400 locations, up from 150 locations two quarters earlier.

Some orders are available for same-day collection, shoppers are offered two-to-four-hour windows for collection and the company charges no additional fees for pickup. Walmart also offers home delivery in a number of areas, but its focus is very much on at-store collection.

Walmart is likely to be taking learnings from its UK subsidiary, Asda, which has a long-established home-delivery operation and has recently pushed into click-and-collect for groceries. It is likely that Walmart has gleaned a lesson from Asda regarding the costs associated with delivery versus collection.

- Euromonitor estimates that Walmart US generated online revenues of $7.24 billion in 2015, equivalent to 2.4% of Walmart US’s total sales and up 19% from $6.09 billion in 2014. These figures include sales of nongrocery items such as toys, electronics and apparel and, given the newness of Walmart’s e-grocery services, nongrocery categories are likely to account for a majority of its online sales. The company says it grew its global e-commerce sales by 12% in fiscal 2016.

Kroger: Also at Nearly 400 Locations

America’s second-biggest grocery retailer, Kroger, has been more cautious still. The company began limited trials of online shopping and collection only in September 2014 and did not officially roll out an online service until August 2015.

America’s second-biggest grocery retailer, Kroger, has been more cautious still. The company began limited trials of online shopping and collection only in September 2014 and did not officially roll out an online service until August 2015.

Kroger’s merger with Harris Teeter in January 2014 brought the latter’s Express Lane buy-and-collect service into the group. Kroger subsequently launched its own ClickList buy-and-collect service. At the end of the company’s fiscal second quarter of 2017, these services were offered in nearly 400 stores. Unlike Walmart, however, Kroger charges customers a picking fee, of $4.95.

Peapod Likely to Gain Scale from Ahold-Delhaize Merger

The US market has been characterized by a number of pure-play retailers right from the early days, when Webvan (now defunct) became an early mover in online grocery.

The US market has been characterized by a number of pure-play retailers right from the early days, when Webvan (now defunct) became an early mover in online grocery.

Amazon aside, Peapod is the biggest Internet-only retailer in the US. It delivers from stores operated by its parent company, Ahold Delhaize, and from its own distribution centers. The company operated 211 small, freestanding pickup points at the end of 2015.

Peapod’s coverage spans only the Eastern US, in line with Ahold’s store footprint. The company makes deliveries in Connecticut, the District of Columbia, Illinois, Indiana, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, Virginia and Wisconsin.

Peapod was owned by Ahold prior to Ahold’s merger with Delhaize in July 2016. The merger suggests that there is scope for Peapod to expand its coverage, using Delhaize stores as further picking centers. However, the newly merged company retains a focus on only the Eastern US.

- Euromonitor estimates that Peapod turned over $748 million in 2015, up 15% from $649 million in 2014. Ahold Delhaize does not split out revenues for Peapod, but the company said that the pure play grew sales by 45% in the New York City area in 2015 thanks to increased capacity at its New Jersey distribution center.

Instacart Offers a Capital-Light Way to Sell Online

Instacart is a picking and delivery service that partners with retailers to enable customers to order from stores and have their purchases delivered. Instacart benefits from not holding any inventory, while its retail partners benefit from having a capital-light way to offer shoppers an online service. Retailers that partner with Instacart include Whole Foods Market (since 2014), Target (since 2015) and Publix (since July 2016).

US RETAILERS OPTING FOR LESS-MARGIN-EROSIVE ONLINE OFFERINGS

Home delivery grocery services can hit the margins of store-based retailers hard because of the high costs associated with picking and delivering orders, including the expense of running fleets of delivery vehicles. We have seen this in the UK, where home delivery is the norm for online grocery purchases, but where the fees charged to customers have fallen over time. (See our first report in this series for more on the UK online grocery market.)

With a focus on collection from stores, major US retailers such as Walmart and Kroger are sidestepping the high costs of delivery. Moreover, those partnering with Instacart are not only opting for a less-capital-intensive service, but also have greater flexibility to opt out of the channel or switch their online offering to another format than they would have if they invested in their infrastructure for servicing orders.

US grocers appear to be striking a balance between tapping a growth channel and avoiding a major hit to profitability, which may be one reward for their slowness in venturing online. American retailers have been able to consider the mistakes grocers have made in more mature markets, where many rushed into the online channel at almost any cost.

KEY TAKEAWAYS

- The US online grocery market is set to boom, driven by major retailers such as Walmart and Kroger changing how shoppers use the channel.

- A substantial proportion of American consumers are already buying groceries online. The main reasons e-commerce accounts for only a tiny share of the market is that average basket sizes are small and online shoppers make grocery purchases infrequently.

- Reflecting this, surveys show that Amazon Prime is the most popular choice for purchasing groceries online. Prime orders are dispatched through the regular mail and items may be sent one at a time, so this service is not suitable for a conventional, full-range grocery shop.

We expect the online grocery market to grow as consumers’ online grocery shopping behaviors begin to more closely echo their in-store behaviors. As they start to use the channel for regular, big-basket shopping trips, e-commerce’s share of total grocery sales will grow.

Read our Online Grocery Series: The UK – A Battle For Profitability report here.