DEEP DIVE: Renting and Retail in the UK: Shifting Property Market Set to Impact on How Shoppers Spend

KEY POINTS

The UK is seeing more people rent rather than buy a home, as rising housing costs are pricing many potential first-time buyers out of the residential property market. This report looks at the key impacts we are seeing, and will see in future years, on the retail sector and consumer spending as a result of more renters.

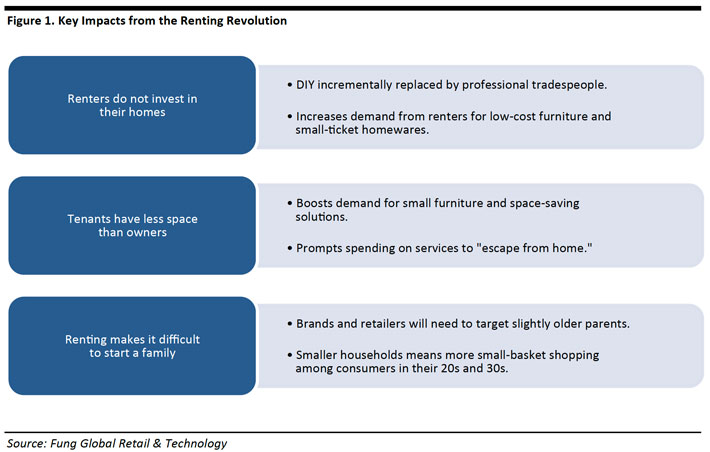

- Renters do not invest in their homes: Home-improvement stores will need to skew their offerings toward professional tradesmen, while small-ticket homewares and low-cost furniture are likely to appeal to renters.

- Tenants have less space than owners: We expect this to boost the market for small furniture and space-saving solutions, as well as underpin growth for spending on services—as renters look to “escape from home.”

- Renting makes it difficult to start a family: The average age of mothers is being pushed up, and this will impact on the shape of the maternity and baby-product markets and likely suppress demand for traditional big, family shopping trips amongst those in their 20s and 30s.

EXECUTIVE SUMMARY

Rising UK housing prices are driving many potential first-time buyers out of the residential property market, and this means that ever-more people are renting the homes in which they live.

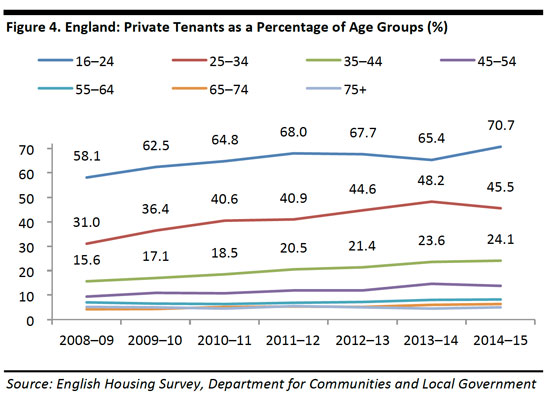

In 2015, some 36.5% of the UK population was renting their homes, up from 30% in 2005. The biggest shift toward renting has been seen among age groups at the younger end of the scale. The proportion of those aged 25-34 that rent from private landlords rose by around 50% between 2008-09 and 2014-15, to reach 45.5%. The proportion of those aged 35-44 that rent privately jumped by more than half to reach 24.1% in 2014-15.

Even if most renters eventually get on the housing ladder, the shifts in the property market have created a larger body of tenants, as people are renting their homes for longer.

We identify the following impacts on the retail sector and on consumer spending as a result of this shift.

Conclusion:

One trend unifies the three themes that we discuss in this report: renting means more consumers are deferring responsibility and retaining the shopping and spending habits of young people for longer.

INTRODUCTION

The way Brits live is changing: more and more British consumers are becoming tenants rather than homeowners. Priced out of buying their first home, ever-more people in their 20s and 30s are becoming long-term tenants. While many of these renters will eventually get on the property ladder—though at an older age than previous generations—many look like they will be renting for life. They are “Generation Rent,” as the media have dubbed them.

In this report, we explore key impacts for the retail sector and consumer spending that we are seeing, and will see in future years, as a result of more renters. We focus on the three themes outlined below:

- Tenants do not invest in their homes.

- Tenants have less space than owners.

- Renting makes it difficult to start a family.

Before that, the first section of this report details the numbers behind the UK’s “renting revolution.”

1. THE RENTING REVOLUTION

Housing Becomes Less Affordable

A boom in buyers from overseas, low interest rates boosting asset prices, high immigration levels, a paucity of social housing and restrictive planning laws have conspired to fuel a surge in UK housing prices.

The result is that more potential first-time buyers are being priced out of the UK residential property market. In turn, this means that ever-more people are renting the homes in which they live.

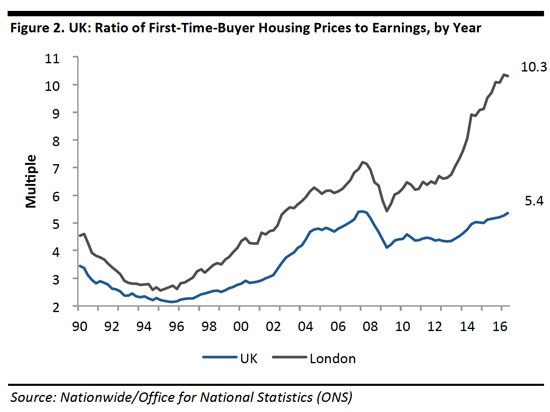

Nationally, as of 3Q16, the ratio of average first-time buyer property prices to average earnings matched the pre-recession peak of 5.4. The ratio has never risen above this level in Nationwide Building Society’s dataset, which runs back to 1983. As of 3Q16, just five of the 13 UK regions had a ratio of less than four times earnings to housing prices.

The national picture is overshadowed by London, where the average first-time-buyer home is now more than ten times the average salary. This is also a record high.

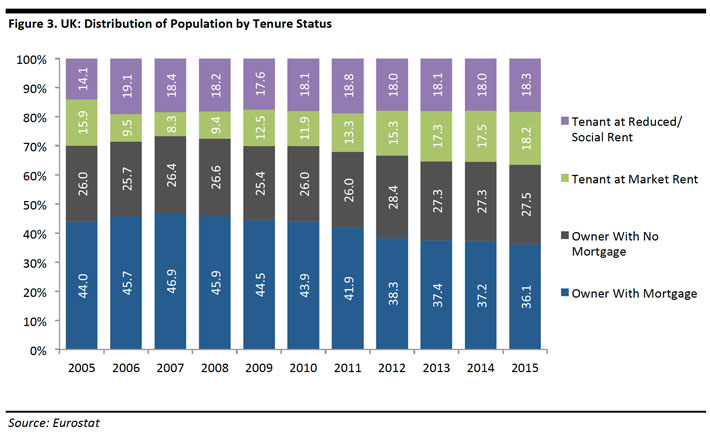

The effects of this are evident in the breakdown of housing tenure. In 2015, some 36.5% of the UK population was renting their homes, up from 30% back in 2005. The private rented sector has mopped up the share lost from home ownership; the proportion of Brits living in social rented housing has remained broadly level (excluding a blip between 2005 and 2006).

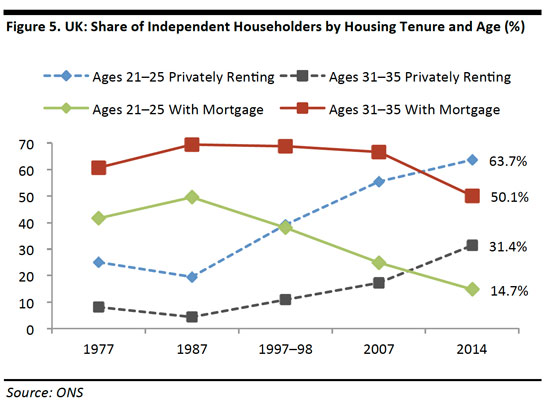

Private Renting Booms Among Younger Age Groups

The biggest shift toward renting has been seen among age groups at the younger end of the scale, further confirming that the growth in renting is being driven by potential first-time buyers being priced out of the market.

The proportion of those aged 25-34 that rent from private landlords rose by around 50% between 2008-09 and 2014-15. The proportion of those aged 35-44 that rent privately jumped by more than half.

A longer view from a different source underlines the structural nature of this shift toward renting. The share of those in their early 30s that are privately renting, for example, is now triple (or more) what it was in the 1970s, 1980s and 1990s.

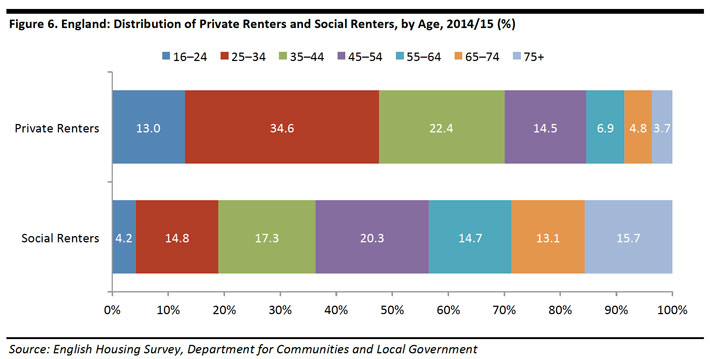

The private rented sector is now skewed heavily toward those aged under 45. The social rented sector sees a much more evenly distributed age profile with a substantial presence of older people, reflecting how much more accessible social housing was for previous generations.

The private rented sector is now skewed heavily toward those aged under 45. The social rented sector sees a much more evenly distributed age profile with a substantial presence of older people, reflecting how much more accessible social housing was for previous generations.

Many renters will eventually get on the property ladder, albeit at an older age than previous generations. However, many more than in previous generations look likely to be renting for life. They have been dubbed “Generation Rent,” by the media.

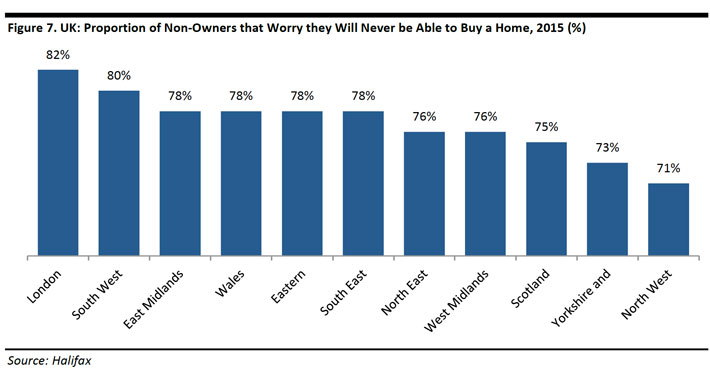

Across all regions, a high proportion of non-home-owners worry about never being able to buy a home, according to a 2015 survey by Halifax bank.

2. THE IMPACT ON CONSUMER SPENDING

Whether or not renters eventually get on the housing ladder, the shifts in the property market have created a larger body of tenants, as people rent for longer periods. In this second section of the report, we look at the impact this is having, and will have in the years ahead, on the retail sector and on consumer spending patterns more broadly. We identify the following themes that will drive changes in spending patterns:

- Tenants do not invest in their homes: Home-improvement stores will need to skew their offerings toward professional tradesmen, while small-ticket homewares and low-cost furniture are likely to appeal to renters.

- Tenants have less space than owners: We expect this to boost the market for small furniture and space-saving solutions, as well as underpin growth for spending on services—as renters look to “escape from home.”

- Renting makes it difficult to start a family: The average age of mothers is being pushed up, and this will impact on the shape of the maternity and baby-product markets and likely suppress demand for traditional big, family shopping trips among those in their 20s and 30s.

Renters Do Not Invest in Their Homes

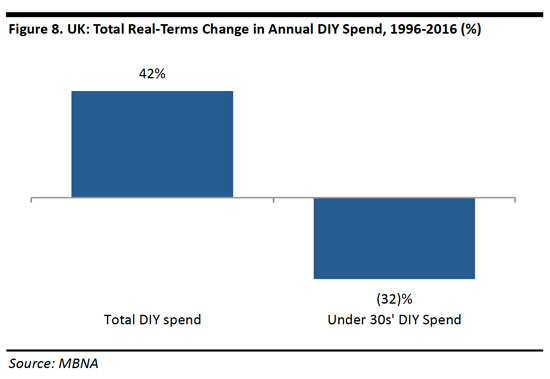

There is little or no incentive for renters to spend on home improvements, and their tenancies may even explicitly forbid this. As a result, we expect the growth in renting to fuel a gradual shift from do-it-yourself (DIY) to professional tradespeople undertaking home improvements on behalf of landlords.

According to MBNA data, over the past 20 years, the UK has already seen a major decline in DIY spend among consumers aged under 30, likely driven by the changing housing market.

Elsewhere in big-ticket home-improvement, we see the renting trend potentially impacting on the furniture market. For those who are renting unfurnished properties, or who need to buy additional furniture in a furnished property, there is likely to be little reason to invest in quality and longevity: they may need to disassemble or even dispose of the item the next time they move.

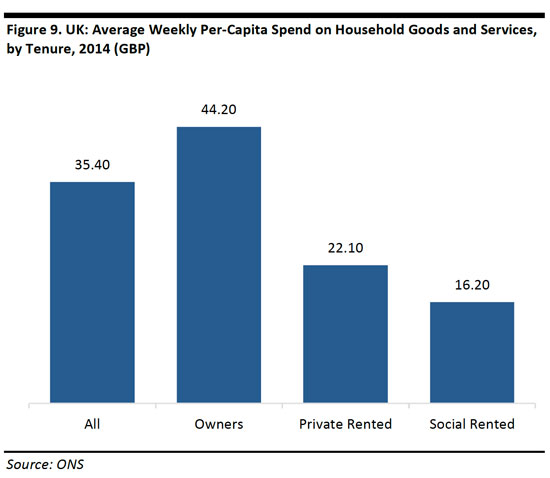

Data from the ONS’s Family Spending dataset show how much less renters typically spend on household goods and services—which includes furniture, DIY tools and household maintenance.

Implications

Trade-Focused DIY Stores Set to Gain Share

DIY stores that cater to professional customers look set to outpace the market, as landlords turn to tradespeople to maintain and repair their properties.

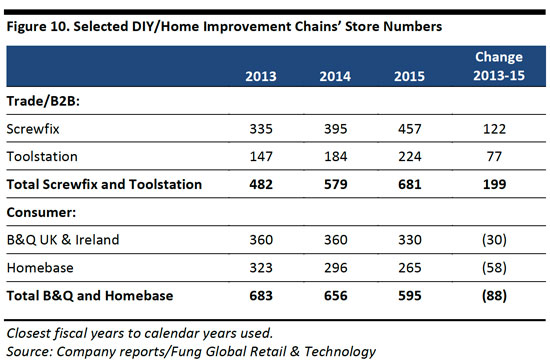

We already appear to be seeing this shift underlying the store expansion and strong comparable growth being seen at chains such as Screwfix; this Kingfisher-owned, trade-positioned retailer posted comps of 14.7% in 1H16, well ahead of Kingfisher’s consumer-focused chain, B&Q, which reported comps of 6.7%.

Below, we show the expansion among two major business-to-business (B2B) banners, Screwfix and Toolstation, and the portfolio contraction among the leading consumer-focused DIY chains, B&Q and Homebase.

Germany, which sees a relatively high share of the population rent their homes, possibly offers some indication of the direction that the UK home-improvement sector will move in: many of the big German DIY chains are targeted as much toward professional tradespeople as they are toward DIYers. Despite the established competition, Kingfisher has been opening Screwfix stores in Germany since 2014, indicating the strength of trade demand in that country.

Smaller-Ticket Homewares and Lower-Value Furniture Likely to Outperform

While DIY may be hit, we see opportunities for smaller-ticket home furnishings categories to capture spending by renters. People who rent homes may not invest large sums in their homes, but they will still likely buy categories such as homewares and small decorative items. Items from these kinds of categories can be taken easily from house to house, are complementary to furnishings that may be provided by landlords and tend to carry a lower ticket price, which means there is less investment by the consumer.

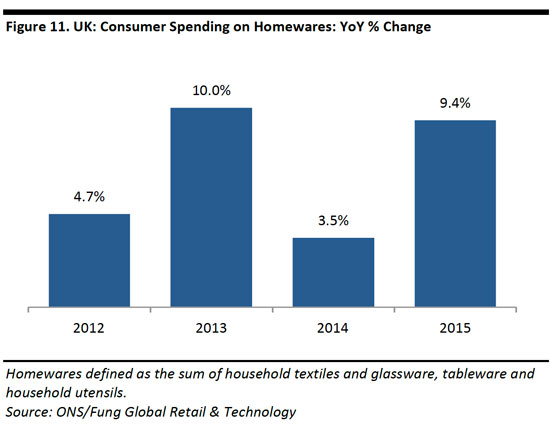

Already, the UK has seen a strong performance in homewares categories: Brits spent £12.5 billion on these products in 2015, up 9.4% year over year. The strength of these categories cannot be pinned solely to the growth in renting; the buoyancy of the overall residential property market is a major factor. However, we expect the category to be supported by housing trends in the years ahead.

We are less bullish on the prospects for bigger-ticket home furnishings. Renters who need to furnish their homes are likely to find lower-cost furniture more appealing than higher-value, longer-lasting investment pieces. Renters may need to move homes more often, may face some uncertainty over when they will need to move or may find themselves moving between furnished and unfurnished properties. As a result, they may find that flat-pack furniture or furniture that is cheap enough to dispose of when moving offers them the flexibility they need.

Moreover, in furnished rental properties, many landlords will look to buy cheaper furniture, instead of seeking out quality furniture as an investment. In an owner-occupied home, the person who buys the furniture benefits from the enjoyment of a quality product; in a furnished rented home, the benefit to the person who buys the furniture is in minimizing cost.

Tenants Have Less Space

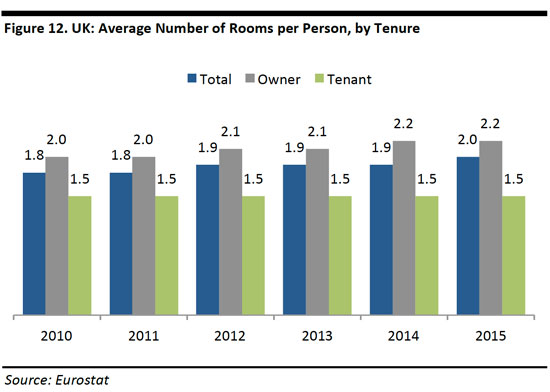

British homes are already small by international standards. And, on average, tenants have even less space than homeowners.

In 2015, the typical renter enjoyed the use of 1.5 rooms at home compared to 2.2 rooms for the average homeowner, with the difference possibly explained by flat-sharing among renters. Moreover, while homeowners have benefitted from an upward trend in the number of rooms in recent years, tenants have seen their average space remain flat.

Implications

Smaller Furniture Sales are Growing

UK retailers are seeing a “growing appetite for multi-purpose storage, compact furniture and practical features,” according to department-store chain John Lewis in its annual How We Shop, Live & Look report for 2016. The retailer noted that Britain’s homes are the smallest in Europe. Data from ShrinkThatFootprint.com show the average UK new-build home is 76 square meters, versus 109 square meters in Germany, 112 square meters in France and 201 square meters in the US.

John Lewis also noted an increase in “Quiet Mark”-certified appliances, as open-plan living means the barriers between the kitchen and living room are broken down. This may be more relevant for tenants, as some landlords convert the traditional living room into an additional bedroom, leaving the kitchen as the main shared space for tenants.

At the same time, as we noted earlier, many renters will be unwilling to pay higher prices: given the more transient nature of renting, they will be looking for low-cost options in categories such as furniture and appliances.

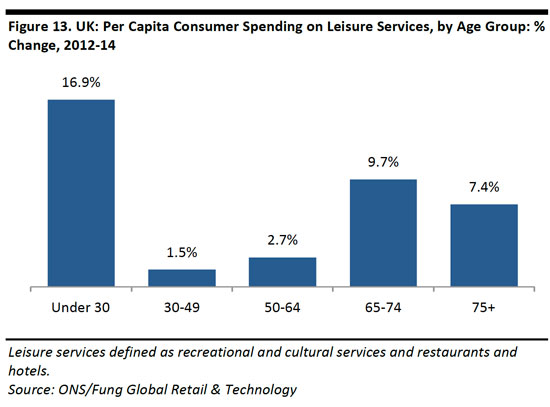

Leisure Services Well Positioned to Benefit

Squeezed into smaller spaces, and often sharing with flatmates, we think renters are more likely than homeowners to seek experiences outside of the home—they are more likely to want to “escape from home.” So, we see leisure services, such as dining out, travel, cultural events and entertainment, standing to benefit from the renting revolution.

Between 2012 and 2014, the average consumer aged under 30 grew his or her spend on leisure services by nearly 17%, we calculate from the ONS’s Family Spending dataset. While this cannot be attributed directly to renting, we think the shift in the way younger consumers live may have played some part.

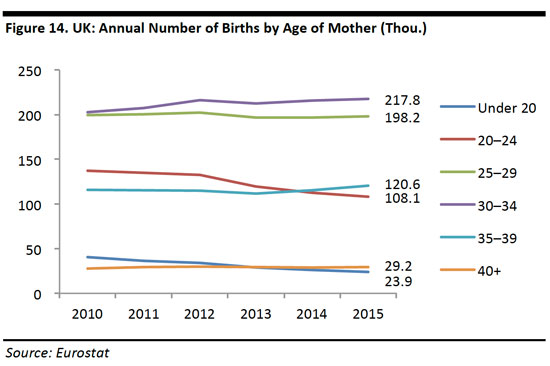

Renting Makes it Difficult to Start a Family

Renting can even impact on birth rates. For some people, the insecurity of living in a rented home means putting off having children: many prospective parents will prefer to be domestically settled before they start a family.

As we chart below, there is a clear medium-term trend for younger women to have fewer children and relatively older women to have more. In terms of the annual number of births, recent years have seen women aged 40+ overtake those aged under 20, and women aged 35-39 overtake those aged 20-24.

According to the EU’s data body Eurostat, the average age at which a UK woman gives birth rose from 28.5 years in 2000 to 30.2 years in 2014 (latest).

Our data do not directly link this to greater renting, but we expect it to be one factor in this trend.

Implications

Impacting on Baby Categories Market

Any shift to lifetime renting, rather than eventually buying a home, could dent the UK’s total birth rate. In turn, this would put a damper on the growth of the baby and maternity products market.

Whether or not total birth rates will decline, the renting culture certainly looks likely to continue pushing up the average age of motherhood. For companies selling baby or maternity products, this means targeting slightly older parents than in the past. And this suggests that brighter prospects lie ahead for those retailers with baby, kids or maternity ranges that target parents in their 30s, such as Next, than for those that target consumers in their 20s, such as H&M.

Smaller Households Means Smaller Baskets Among Younger Shoppers

Later parenthood means households headed up by people in their 20s and 30s are more likely than in the past to be smaller households. In turn, this suggests these consumers are more likely to be small-basket shoppers with less demand for big stores designed for large families.

These demographic trends look set to underpin existing fast-growing segments such as convenience stores and small supermarkets. They will compound problems for large superstores, which rely on pulling in family life-stage shoppers, and retaining their loyalty once children leave home. At the same time, the generally more limited space that tenants have at home, which we noted above, provides further support for this small-basket shopping trend.

In short, deferred parenthood means renters will retain the convenience-driven, impulse-heavy shopping habits of younger people for longer.

KEY TAKEAWAYS

We think one trend unifies the three themes that we have discussed in this report: renting means more consumers are deferring responsibility and retaining the shopping and spending habits of young people for longer.

- Renters are passing the responsibility of home-maintenance, and often big-ticket purchases, to their landlords.

- Tenants look likely to spend on services as a means of enjoying life outside of the home.

- Renters are likely to defer starting a family, with the associated impact on shopping behaviors.