DEEP DIVE: UK Retail Overview: Characteristics, Developments and Prospects

KEY POINTS

This is the fourth in our series of reports analyzing retail trends in major economies. Here are the top trends we have identified in the UK retail sector:

- UK shoppers appear to be prioritizing spending on services at the expense of retail. Apparel stores appear to have been particularly hard hit by this trend.

- Discount retailers are now seeing underlying sales growth slow, following several years of rapid growth. Future top-line growth among discounters will likely be driven by new store openings.

- Internet-only retailers are outperforming multi-channel retailers online, despite brick-and-mortar retailers having poured cash into their online propositions.

- We think there is more potential for sustained growth among Internet pure plays than there is among store-based discounters.

- The grocery sector has seen a fragmentation of sales away from larger stores, and this looks set to continue. Amazon’s entry into the grocery market adds further pressures.

- Following the UK’s vote to leave the EU, British consumers have displayed resilience, and there has been no perceptible negative effect on retail demand.

EXECUTIVE SUMMARY

The UK: A Fast-Changing Retail Sector

This is the fourth in our series of reports analyzing retail trends in major economies. Our previous reports looked at Germany, France and Turkey, and they can be found on our website, FungGlobalRetailTech.com.

UK retail is dynamic, diverse and innovative. The country leads the Western world in terms of e-commerce penetration, its retailers have pioneered multi-channel services such as click-and-collect and it is the home of innovative Internet-only retailers such as ASOS, boohoo.com, AO World and Ocado. The UK retail sector has seen much upheaval in recent years, not only because online sales have boomed, but also because an explosion in the discount segment has resulted in higher standards in budget retailing. At the same time, the sector has enjoyed several years of solid growth—although, as we discuss below, this growth has softened in 2016.

Here are the top six trends we have identified in UK retail:

1. A renewed prioritization of services over retail: Nonfood retailers, and especially apparel stores, are seeing growth slow or even turn negative, and consumers’ increased spending on leisure services appears to be one reason for this. We see this leisure spending as being driven in part by the pressures of social media and in part by the greater ease of finding and booking services via mobile apps and online aggregators.

2. The slowing of the discount boom: Discount retailers that made much headway in recent years are also now seeing underlying growth slow or turn negative. These include Primark, Sports Direct, B&M and Poundland, and there is speculation that privately owned Aldi is now seeing flat comps. In the coming period, top-line growth in the discount segment is likely to be driven by new store openings rather than by robust underlying growth.

3. Internet-only retailers are outperforming multi-channel retailers in e-commerce: Despite brick-and-mortar retailers making substantial investments in their e-commerce capabilities, they are losing share in the online channel to Internet pure plays.

4. There is more growth potential in online pure plays than there is in the store-based discount segment: We see more opportunities for sustained, strong growth among Internet pure plays than among store-based discount retailers. And we see discount demand in categories such as apparel increasingly migrating to sites such as boohoo.com, Missguided and Amazon. We estimate that e-commerce could be capturing roughly 30% of apparel sales and around 9–10% of grocery sales in five years’ time.

5. The grocery shopping basket has fragmented to multiple retailers and formats: Discounters, convenience stores, local supermarkets and specialists have gained from consumers’ shift to buying when and where they need to rather than making a single big weekly shopping trip. Meanwhile, nonfood categories and big-basket grocery retailers continue to migrate online. These trends have dented margins, undermined the profitability of large grocery stores and left large-store retailers facing an excess of space.

6. Brexit: Brits have exhibited resilience following the Brexit referendum on June 23. Consumers have continued to shop in stores and buy houses, while businesses have continued to hire. We see structural shifts, such as those noted above, as having much more impact than the Brexit vote on retail in the near term.

The subsequent sections of this report consider these trends in more depth.

1. SPENDING ON SERVICES APPEARS TO HIT RETAIL

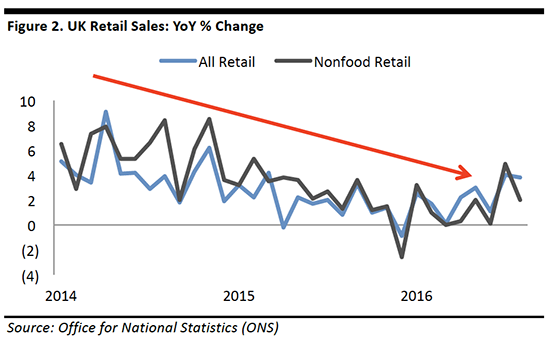

UK retail enjoyed a period of buoyant growth from 2010 through 2014. An overall healthy economy with low unemployment and the return of real wage growth (albeit slow growth that was weighted toward the end of this period) helped the sector. But so, too, did Brits’ willingness to spend: even at points when real wage growth was contracting, retailers were enjoying robust growth in sales.

Despite the strengthening health of the UK consumer, the environment weakened in 2015, and lackluster demand at nonfood retailers dragged down overall sector growth. This resulted in the lowest reported December retail performance in a quarter of a century—and the weakness has continued in 2016.

There have been signs of improvement in the most recent monthly data, but we suspect this is partly because the depreciation of the British pound has flattered the overseas sales of major British retailers (in those instances where they are included in the aggregate sector data).

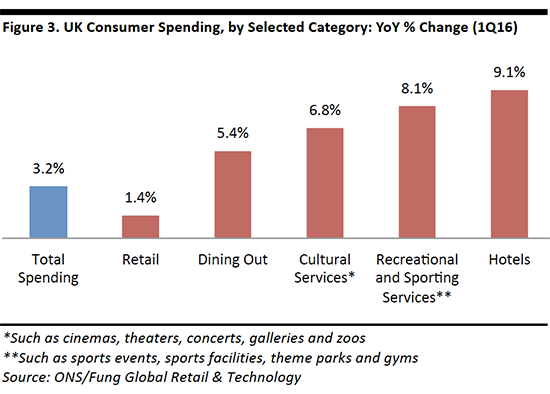

We think one reason for the weakness is that Brits are prioritizing spending on leisure services over physical products. The hotels sector and the recreational and sporting services sector—which includes tickets to sports events, visits to theme parks and gym memberships—were the standout services sectors in the first quarter of 2016 (latest available data).

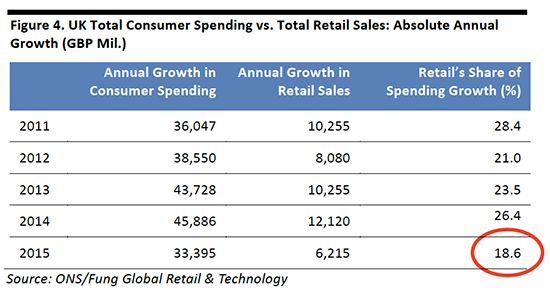

The retail sector captured just 18.6% of the total increase in consumer spending in 2015—a lower share than in any recent year. In 2014, for instance, retail captured more than a quarter of the total annual growth in spending.

WHY ARE SHOPPERS SPENDING ON SERVICES INSTEAD OF RETAIL?

We see two major elements driving consumers to spend on leisure services rather than on goods:

- First, the growth of social media—and particularly the boom in photo and video content on sites such as Instagram and Facebook—is likely playing a role. Younger consumers tend to enthusiastically document their lives on social media, which arguably puts pressure on them to be seen traveling, attending concerts and sports events, dining out, and enjoying other leisure activities. The result is what we call “the Instagram effect” on consumer spending, with services gaining at the expense of retail.

Second, mobile connectivity is making it easier to find and book leisure services, including weekend getaways, salon treatments and last-minute dinner reservations. Apps such as YPlan allow consumers to discover leisure events and activities in their city, and online and app-based booking intermediaries—such as Just Eat, Deliveroo, UberEATS and Amazon Restaurants in food service—are making it easier to spend on services. This is particularly important in sectors where fragmentation has traditionally made it difficult to find and book services.

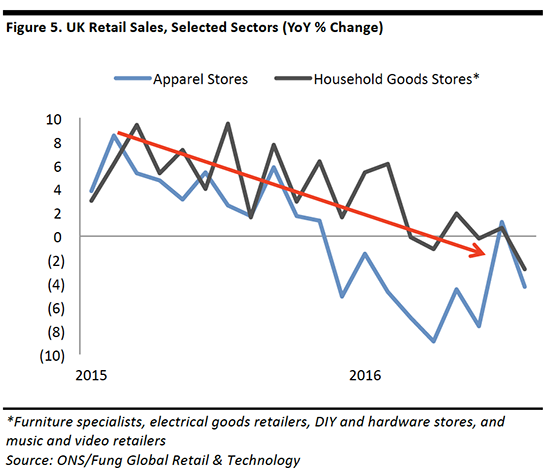

APPAREL RETAIL BEARS THE BRUNT

Some sectors have proven resilient: the mixed-goods/department store sector, for instance, has been boosted by the expansion of mixed-goods discounters as well as by the strength of John Lewis’s top line.

Two sectors that have taken hits are apparel specialists and household goods stores. The downturn has been especially sharp at the former, with the sector squeezed not only by weakness in category spending, but also by the sustained rapid growth of pure plays such as ASOS, boohoo.com and, probably, Amazon Apparel and Zalando (although we do not have confirmed UK data for the last two).

The UK’s second-biggest apparel retailer, Next, flagged the hit to the apparel sector earlier this year, when it noted:

There may be a cyclical move away from spending on clothing back into areas that suffered the most during the credit crunch…travel, recreation and going out.

- For more details, see our report UK Apparel Malaise Signals a Shift in Consumer Spending Priorities at bit.ly/FungUKApparel.

2. IS THE DISCOUNT BOOM FADING?

Fragmentation away from middle-ground generalists in favor of retailers with a more specialized positioning has been seen across various retail sectors in recent years. We think it is no surprise that the period from the start of the recession to today is bookended by two major retail failures—and that both retailers were characterized by their generalized, middle-ground propositions:

- Mixed-goods chain Woolworths, perhaps the epitome of generalized retail, shut down in January 2009.

- BHS, an undistinguished, lower-midmarket department store chain, closed its doors for the last time in August 2016.

Middle-ground generalists—from Tesco, Asda and Morrisons in grocery to Marks & Spencer (M&S) and Debenhams in apparel—continue to turn in underwhelming growth as consumers enjoy an abundance of choice from more specialized stores and Internet-only retailers.

The growth of discount (or budget), pure-play and premium retailers has been a trend seen across both food and nonfood retail. Budget retailers, in particular, have been winners, in part because major players, from Aldi in grocery to Primark in apparel, have raised the standards of discount retailing.

Here are some of the success stories in British retail over the last few years:

- Aldi and Lidl in grocery: Aldi UK & Ireland posted a 29.3% CAGR in revenues for fiscal years 2010–2015. No UK-specific accounts are available for Lidl, but market-measurement service Kantar Worldpanel has recorded broadly similar, storming growth for both Lidl and Aldi.

- Primark and Sports Direct in apparel: Primark’s UK division grew revenues at a 7.8% CAGR for fiscal years 2010–2015. Sports Direct turned in a revenue CAGR of 12.7% in the five years through fiscal 2016.

- B&M and Poundland in the mixed-goods discount sector: B&M saw a CAGR of 27.7% in revenues in the four years through fiscal 2016, while Poundland’s revenues grew by a CAGR of 12.7% in the four years through fiscal 2015.

For more on discount channels, see our previous, in-depth reports:

- UK’s Second Grocery Discount Boom at bit.ly/FungUKDiscount.

- European Grocery Discounters: Small Stores, Big Threats? at bit.ly/FungGroceryDiscounters.

- Primark: Primed for the US at bit.ly/FungPrimarkUS.

LIFE IS GETTING TOUGHER FOR DISCOUNTERS

Despite the discounters’ success in recent years, we are now seeing a significant slowing in the segment.

Aldi and Lidl’s sales are slowing. Kantar Worldpanel measures sales of major grocery stores and it has recorded a steady slowing of growth at the discounters. In the 12 weeks ended September 14, 2014, Aldi grew sales by 29.1%, while Lidl grew sales by 17.7%. Fast-forward two years to the 12 weeks ended September 13, 2016, and Aldi grew sales by 11.6% and Lidl by 9.5%.

Moreover, this growth is in the context of aggressive store-opening plans. Sanford C. Bernstein analyst Bruno Monteyne suggested this year that Aldi’s comparable sales had reached zero. Aldi’s UK boss, Matthew Barnes, recently dismissed the “bizarre fascination with like-for-like sales” in an interview with The Telegraph, indicating that the privately owned German discounters are much less concerned with comparable sales growth than their publicly traded peers are.

Primark’s comps have turned negative. Primark recently reported its pre-close statement for the year ended September 17 and it estimates that its comparable sales during the year turned negative, to the order of (2)%. This included a sequential weakening from flat comps in the first half of fiscal 2016 and is reportedly the first time Primark has posted negative underlying sales growth in 16 years. While this is a groupwide figure, and so includes international operations, we think the UK segment may have performed even worse, given the sharp downturn in the UK apparel market this year.

Sports Direct has slumped. Discount-positioned sportswear and casual apparel retailer Sports Direct has posted substantially slowing underlying growth and a slump in investor confidence. In the year ended April 24, 2016, the company’s core sports retail segment posted comps of (0.8)% versus 7.4% comp growth in the prior fiscal year.

Mixed-goods discounters are slowing. The leading listed mixed-goods discounters, B&M and Poundland, have reported similar slowing trends:

- B&M’s latest results, covering the 13 weeks ended June 25, 2016, show that UK comps were flat in the period. In the year ended March 26, UK comps were just 0.3%, down from 4.4% in the prior year.

- For the year ended March 27, 2016, Poundland posted comps of (3.9)%, down from 2.4% in the prior year. (Poundland was recently acquired by retail group Steinhoff International, so we do not have subsequent disclosures.)

IS THIS THE END OF THE DISCOUNT BOOM?

Opportunities remain and a number of discount retailers will continue to take share from middle-ground retailers—but in general these gains look like they will be driven more by new store openings than by robust underlying growth. The low-hanging fruit has now been picked and the era of underlying outperformance for the discount segment appears to be drawing to a close. A maturing discount segment with constraints on physical capacity, heightened competition from Internet pure plays in categories such as apparel and demanding comparatives are among the headwinds the discounters face.

A slowing in the discount segment does not, however, mean the hard-hit generalist, middle-ground segment will recover lost ground: we expect the very middle of the market to continue to find trading tough, with Internet-only retailers among those likely to steal share from legacy chains.

For more on the challenges of the midmarket in the department-store sector, see our report European Department Stores Update: Reviewing Trends and Performance at bit.ly/FungDeptStoresEurope.

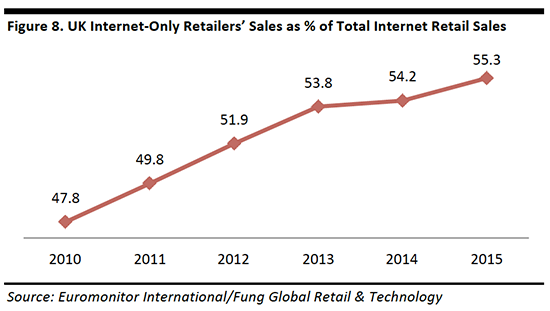

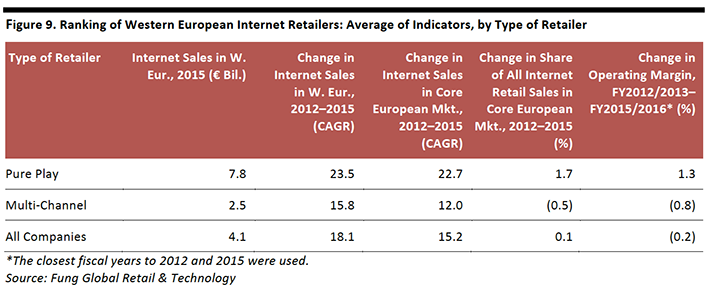

3. PURE PLAYS ARE WINNING GREATER SHARE ONLINE

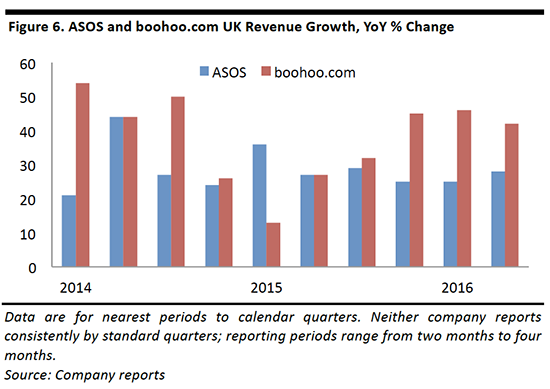

Internet-only retailers comprise one segment that has consistently benefited from the fragmentation of shopping away from middle-ground generalists. While discount brick-and-mortar retailers may be gradually running out of steam, Internet pure plays remain a high-growth threat to established brick-and-mortar chains. The outperformance is most evident at the major apparel pure plays, ASOS and boohoo.com, which appear to be immune to the current slowdown in apparel; in fact, boohoo.com has posted accelerating UK sales growth this year.

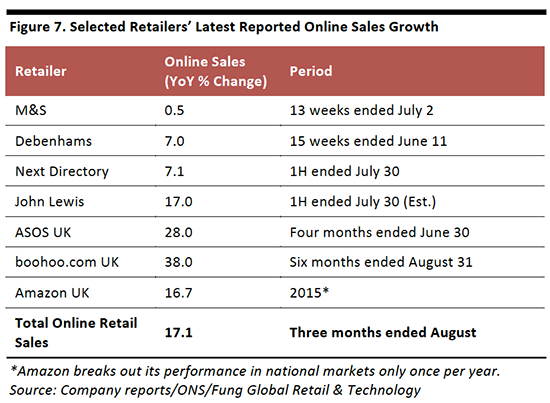

Below, we bring together recent online sales growth figures for major store-based and Internet-only retailers. These figures imply that pure plays are continuing to outpace their multi-channel rivals—even John Lewis, which has long been lauded as the epitome of multi-channel success.

This is not just a recent trend. The medium-term pattern is for Internet-only retailers to gain share of online sales at the expense of multi-channel players.

We recently explored this trend in more detail in our report Identifying E-Commerce Winners: Our Ranking for Western Europe. In that report, we analyzed the performance of Western Europe’s top 20 online retailers, a substantial number of which are UK companies, and our analysis confirmed that pure plays are tending to outperform their brick-and-mortar rivals in the online channel.

Taken from that report, the table below ranks the average performance of the top pure plays against the average performance of multi-channel retailers on five selected metrics, including growth in online sales and change in online market share. This averaged data provides further evidence of the lead enjoyed by Internet-only retailers on a number of metrics of success. Although the data are for Western Europe as a whole, they are indicative of the trends we see in the UK market.

- For more information, see our report Identifying E-Commerce Winners: Our Ranking for Western Europe at bit.ly/FungInternetEurope.

4. MORE GROWTH POTENTIAL FOR PURE PLAYS THAN FOR STORE-BASED DISCOUNTERS

Internet-only retailers are a sustained and major threat to brick-and-mortar players. There is a case to be made that online pure plays will displace discount stores as the principal threat to the major store-based groups in the coming years—although this will vary by sector and by retailer.

Brick-and-mortar discount will see a natural cap on its growth as the market for physical stores nears saturation. Pure plays, by contrast, see no such physical constraint and therefore look to have room for sustained growth across multiple categories.

In categories such as apparel, we see scope for e-commerce pure plays to capture an ever-greater share of discount spend. Sites such as boohoo.com, Missguided and Amazon (which has long established itself as a de facto off-price apparel store) look well placed to capture share at the expense of store-based budget rivals.

Here are some figures that we think underline the robust prospects for e-commerce generally:

- Despite the online channel maturing, UK Internet retail sales have been accelerating, according to recent data from the ONS. From January through August 2015, total Internet retail sales growth averaged 12.8%; for the same period in 2016, such growth averaged 15.1%.

- E-commerce currently accounts for 23% of UK apparel sales, up from 21% last year, according to Kantar Worldpanel. We estimate that the proportion of apparel sales made online could reach 30% in five years, assuming the annual increase in the penetration rate slows to an average 1.5% per year.

- Similarly, we see substantial scope for e-commerce to win share in grocery, given that just 6% of category sales are currently made online but that 48% of consumers are buying groceries online, according to Mintel. We believe e-commerce could grow to account for about 9–10% of total grocery sales within five years as the substantial number of occasional online buyers become more regular online buyers.

- Just 8% of UK furniture sales were made online in 2015, according to Mintel, compared with fully 48% of electrical and electronic goods sales. Given that both categories are predominantly made up of big-ticket, cumbersome, hardline goods purchased primarily based on specifications, we see major scope for online furniture sales to grow rapidly and for e-commerce to gain significant share of total category sales in the coming years. We see the near-50% share captured by e-commerce in electrical and electronic goods as a possible long-term target for the furniture category.

In each of these segments, we expect well-positioned pure plays, such as ASOS in fashion, Ocado in grocery and Made.com in furniture, to outperform their store-based counterparts.

We also see opportunities in the UK market for sharply positioned international pure plays to build share. Companies that currently have relatively small positions in the UK market include Zalando (in apparel), AmazonFresh (in grocery) and Wayfair (in furniture), but these and others could tap demand for shopping at online-only retailers.

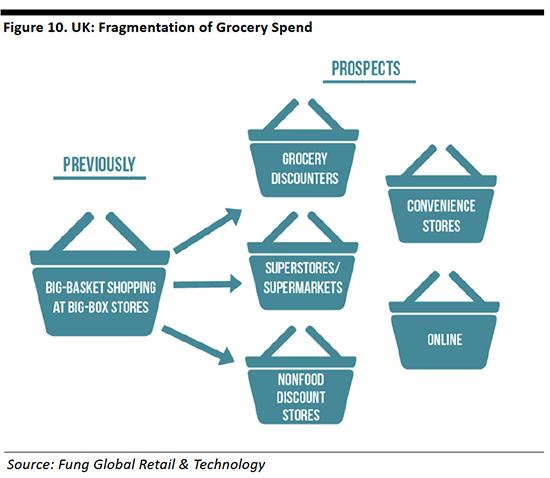

5. FRAGMENTATION HITS GROCERY INCUMBENTS

The grocery sector has its own dynamics and its own difficulties. The underlying theme of the past few years has been fragmentation away from the long-standing tradition of weekly or fortnightly major grocery shops complemented by occasional top-up shopping trips. Instead, there has been a clear trend toward shoppers buying only when they need something and often at smaller stores closer to home.

- Grocery discounters Aldi and Lidl have grown fast, spurred by the ingraining of recession-induced shopping behaviors and enabled by the noticeable softening of their hard discount formats. The limited ranges at discounters have boosted demand for top-up shops from other formats.

- Mixed-goods discounters such as B&M and Poundland have made similar headway, expanding fast and raising standards in the discount sector with a brand-heavy offering that complements Aldi’s and Lidl’s predominantly private-label offering. However, as noted above, growth has slowed at discount stores.

- Major nondiscount grocers Tesco, Sainsbury’s, Co-op Food, Waitrose and M&S have pushed aggressively into convenience-store formats to cater to the demands of faster-living consumers.

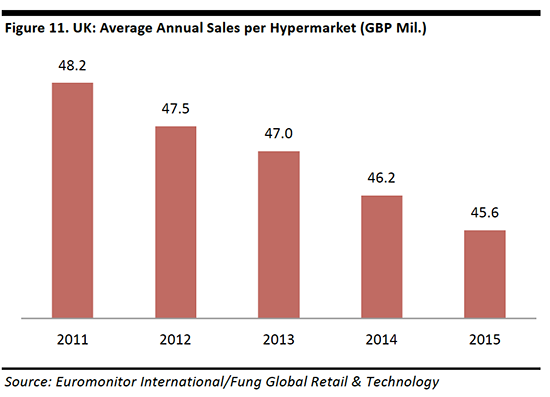

At the same time, Internet grocery retailing has skimmed off some shoppers’ residual big-basket shopping trips. Big-store, nondiscount grocery formats, long the default destination for traditional weekly shopping trips, have been hardest hit by the splintering of shopping into other formats.

Meanwhile, superstores have been further hit by the migration online of nongrocery categories such as electronics, entertainment media and apparel.

We calculate that these changes left the average UK hypermarket generating some £2.6 million (US$3.4 million) less in revenue per year in 2015 compared to 2010; this is equivalent to a 5.5% drop in the annual turnover of each hypermarket.

The incessant chipping away of big-store sales threatens their profitability: with high fixed costs, retail is volume sensitive and grocery operators, in particular, have very slim margins. In the coming years, if the online channel continues to steadily increase its share of total grocery sales like we expect it will, it will represent a sustained threat to the viability of large superstores.

Shoppers’ migration online, coupled with ongoing store openings in discount and convenience formats, will only worsen the capacity problem for UK grocery retail. Major chains such as Tesco and Morrisons are already closing some stores and Tesco, Sainsbury’s and Waitrose have booked write-downs on property pipelines that will no longer be developed. We expect that retreat from excess space will be an ongoing issue for brick-and-mortar grocers in the coming years.

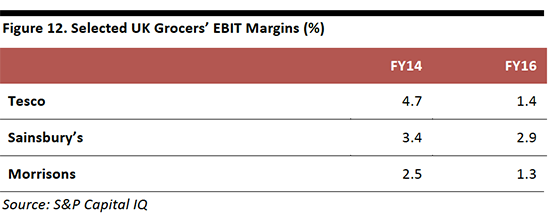

A LESS PROFITABLE SECTOR

Margins at the major grocers have already come under threat, principally from strong price competition in the sector. The growth of discount stores spurred the big grocers to cut prices and shift pricing strategies from promotions to everyday low prices in order to appeal price-sensitive consumers. This resulted in food-price deflation and a deterioration of nondiscounters’ margins, and exacerbated the tumbling of top lines at major grocery chains.

But even if their market-share gains slow radically, the discounters will continue to exert pricing pressures. Meanwhile, the growth of e-commerce will likely add costs over the medium term. In short, the main impacts on margins are not a temporary effect that can be batted away by simply supporting market share: the big grocery retailers are likely to experience sustained downward pressures on their margins.

Decreasing profitability has forced large grocery retailers to refocus their business around their core activities. For instance, Morrisons divested its short-lived convenience-store chain to concentrate on its core estate, while Tesco sold a number of its non-UK grocery operations, including restaurant chain Giraffe, coffee shop chain Harris + Hoole, Turkish retailer Kipa and Dobbies Garden Centres.

AMAZON PRESENTS A NEW THREAT

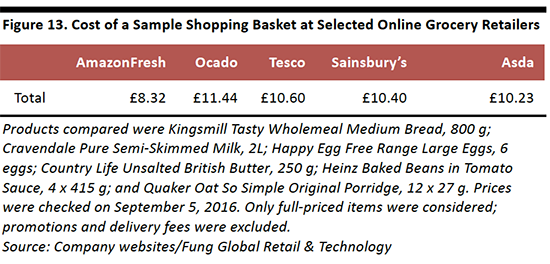

Heaping further pressures on an already hard-hit sector was the June 2016 UK launch of Amazon’s grocery shopping service, AmazonFresh. The service launched in a number of London postcodes, and has since been expanded, offering Amazon Prime members same-day delivery in one-hour slots for orders placed before 1 pm.

Amazon pressures competitors not only through the immediacy of its fulfillment, but also on prices, and Amazon’s currently look to be among the lowest in the market. We compared the prices of a handful of popular branded grocery products from AmazonFresh and four other online supermarkets. A consumer shopping for the basket at AmazonFresh would save £1.91 (US$2.49) versus purchasing the same items via Asda’s site and £3.12 (US$4.06) versus purchasing the basket through Ocado.

For private-label and fresh products, meanwhile, Amazon has the security of a supply deal with the UK’s fourth-largest grocery retailer, Morrisons. This gives Amazon a jump-start in these categories, removing the need for it to build its own private-label offering in the near term.

While Amazon’s presence in UK grocery is currently negligible, the coupling of its strong price proposition with rapid fulfillment will only intensify the margin pressures on long-established chains.

6. AND BREXIT?

Finally, we turn to the issue of Brexit. There is one reason why we have left this theme until last: the country’s decision to leave the EU has so far had no apparent impact on the consumer economy. Brits have exhibited tremendous resilience following the referendum of June 23. Consumers have continued to shop in stores and buy houses, while businesses have continued to hire.

Retail sales, in particular, have strengthened in the months since the referendum. Some commentators have speculated that tourist shoppers are driving this growth, due to the devalued pound. However, in August, two sectors that saw substantial improvements in sales growth were grocery stores and Internet pure plays—and neither of these is a significant destination for tourist spending.

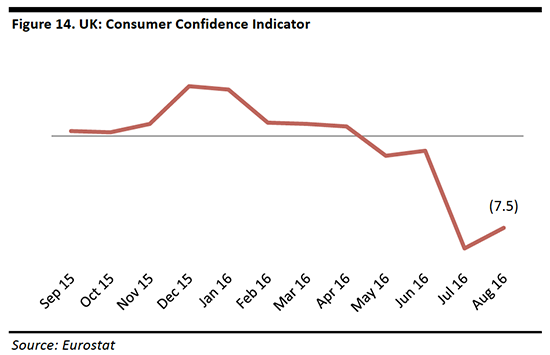

The immediate postreferendum period did see a decline in consumer confidence. However, this was unsurprising given the volley of negative statistics with which Brits were bombarded by the “Remain” campaign during the run-up to the referendum. Brits were warned of recession, falling house prices, higher shop prices, mass job losses, lower pensions, a weakened National Health Service, “a decade of uncertainty” and even world war, should they vote for Brexit. But the consumer confidence index returned to an upward trend in August (latest available).

The minimal short-term effects of the referendum have resulted in a raft of upward revisions to estimated economic growth for 2016 and 2017; in the immediate aftermath of the vote, economists had issued doom-laden forecasts. Bodies such as the Organisation for Economic Co-operation and Development have been forced to row back on their previous economic downgrades.

The UK’s exit from the EU is likely to be a couple of years away, and the shape of the agreement negotiated between now and then will determine its economic and consumer effects. Given that there are so many unknowns, there is little value in attempting to forecast specific effects from the exit—not least because we have recently seen how inaccurate economists’ forecasts can be even in the near term. For now, consumers are willing to spend, and this is reassuring news for retailers and other consumer-facing companies.

- We have published a series of Brexit reports, which can be found on our website, FungGlobalRetailTech.com.

KEY TAKEAWAYS

Here are our main takeaways on the UK’s fast-changing retail sector:

- UK retail enjoyed robust growth in the postrecession years, but 2016 has seen a downturn in nonfood retailing, led by a decline in sales at apparel stores. Consumers appear to be prioritizing spending on leisure services.

- Middle-ground retailers have suffered from the rapid growth of more sharply positioned competitors. These competitors include grocery discounters, mixed-goods discounters, low-price apparel stores and Internet pure plays.

- However, the boom in budget stores is slowing noticeably. In the coming years, we expect the market-share gains made by discount retailers to be driven by new store openings rather than by underlying growth.

- This does not mean life will get much easier for midmarket generalist retailers, in part because Internet-only retailers present a sustained threat to established chains.

- Internet pure plays are gaining share of total online retail sales, despite brick-and-mortar chains pouring money into multi-channel propositions. We expect online pure plays to drive e-commerce’s increasing share of sales in categories such as apparel, grocery and furniture. And we see opportunities for international pure-play retailers to tap this British demand for online shopping.

- Brexit is having surprisingly little near-term impact. The most important factors in retail are structural shifts such as those we outlined above.