DEEP DIVE: The Changing Retail Landscape & The Evolving Opportunity For Better Demand Planning

KEY POINTS

- We see an increasing disconnect between the proliferation of multiple distribution channels and some of the demand-planning models that were built around supplying goods to brick-and-mortar stores.

- Demand planning affects inventory planning, which feeds into a retailer’s return on capital. We examine the financial data of publicly traded retailers across different product verticals, and conclude that efficient demand planning is particularly important for the apparel and footwear industry.

- We recommend that retailers adopt sophisticated demand-planning solutions to better align their inventory plans and purchasing decisions with their customers’ demands.

- In this report, we introduce the more prominent demand-planning solutions available on the market. We also highlight successful cases of apparel retailers that have leveraged the technologies of 7thonline – a provider of cross-channel merchandise management solutions to the Apparel, Footwear, and Accessories (AFA) industry – in fulfilling their demand-planning strategies.

EXECUTIVE SUMMARY

Retailers are faced with an increasingly complex retail environment, driven by strong demand for e-commerce, more sophisticated consumer preferences, increasing channel complexity and intensifying competition. We see an increasing disconnect between the new norms of consumer retail and some of the supply-chain and demand-planning models that were built around supplying goods to brick-and-mortar stores. The challenge is exacerbated for retailers that have to match demand and supply across multiple channels (owned stores, wholesale, online and franchised stores) and fashion retailers, which typically have shorter product lifecycles.

Externalities are the primary reason why retailers that have to match demand and supply across different channels are more exposed and in need of better demand-planning processes. In addition to the direct-to-customer business, these retailers typically depend on their wholesale and franchisee customers for consistent and trustworthy demand plans.

We recommend that retailers adopt sophisticated demand-planning solutions to better align their supply-chains operations and their customers’ needs. Sophisticated demand-planning solutions help integrate inventory plans, demand forecasts and purchasing decisions to meet customers’ demands. As demand-planning decisions need to be anchored on more scientific approaches, applications that integrate planning, buying, allocation and predictive analytics in real-time are seen as powerful alternatives to spreadsheets.

The transition to better demand-planning solutions will enable retailers to create a single, firm-wide view of demand by consolidating demand plans across their owned-store, wholesale and e-commerce channels. Moreover, better demand planning will lead to an improvement in forecast accuracy that is more responsive to demand signals in real-time. This is consistent with a notable shift of retailers’ supply chains to demand-driven supply chains (DDSC), rather than merely reactive systems.

Better demand planning enables retailers to provide wider product availability and be responsive to customer needs in a cost-effective way. Studies indicate that retailers with higher demand-planning maturity have demonstrated better operating and financial results, including higher sales, lower operating expenses, lower inventory holdings and faster inventory turnover.

Demand planning affects inventory planning, which feeds into a retailer’s the return on capital. We examine the financial data of publicly traded retailers across different product verticals and distribution models. We conclude that efficient demand planning is particularly important for the apparel and footwear (AFA) industry.

In the final section of the report, we introduce the most prominent demand-planning solutions vendors. We also highlight successful case studies in the apparel industry that have leveraged the technologies of 7thonline – a provider of cross-channel merchandise management solutions to the AFA industry – which helped these retailers fulfil their demand-planning strategies.

INTRODUCING DEMAND PLANNING

Demand planning refers to the business process of predicting future demand for products, and then aligning production and distribution capabilities accordingly. The end result is to create a demand plan aligned with financial goals and inventory plans. The process involves the sharing of timely data, accurate processing of this data and agreement from various business functions on joint business plans along the supply chain.

Sophisticated demand planning would help a supply chain achieve its goal of delivering the right product, at the right time, at the right place and at the right price. A customer-oriented demand-planning process will allow for ample inventory levels to meet immediate demand, and future demand projections driven off predictive analytics.

OUR EXPECTATIONS FOR THE EXTERNAL CONSUMER RETAIL ENVIRONMENT

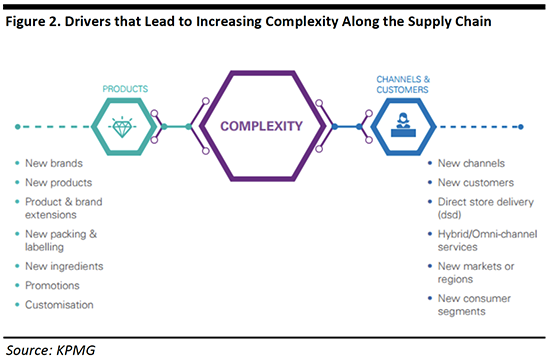

We expect the evolving norms of the consumer retail environment to drive an increased urgency for better demand-planning solutions for retailers. Today’s retail landscape engenders greater complexities which the conventional demand-planning models can no longer adequately cope with. Digital disruption (particularly on the demand side) has given rise to changes in the retail landscape, such as new competitors, more sophisticated consumers and new distribution channels which retailers are pitted against. Themes we explored include: 1) the need for retailers to constantly evolve;

2) growing alternatives for consumers from the emergence of online retailers; 3) how distribution is impacted from “on-shelf availability” to “on demand availability”; and 4) how the added complexity of sourcing from and selling to emerging markets increases globalization.

1. Retailers – the Need to Constantly Evolve

With the emergence of multi-channel retailers, incumbent physical retailers need to constantly adapt to stay relevant. The new breed of retailers they are pitted against is nimble across multiple channels, is introducing a larger variety of merchandise and turning over inventory at a faster pace and with more sophisticated fulfilment.

Moreover, the broader retail landscape has become more complex – retailers are operating in an increasing number of locations, with more business units, more manufacturing sources and shorter product life cycles, and are selling to more markets in which consumers have diverse tastes.

2. Consumers – Growing Alternatives with the Emergence of Online Retailers

Changes in consumer demand are driving the need for better demand planning. Consumers now expect greater convenience, faster speed, more customized orders and more frequent order changes. Retailers are obliged to offer more flexible return policies and more product choices to fast-changing consumer tastes, yet at the same time, maintain aggressive pricing in order to stay relevant with the consumers they sell to. This all necessitates better demand planning.

In addition, retailers need to adapt to more volatile and uncertain global consumer demand, which has become more pronounced following the global financial crisis, and resulted in reduced demand visibility for retailers. Global uncertainties (sharp currency fluctuations, financial and commodity market volatility, divergent monetary policies across leading economies) have hindered a recovery in consumer confidence and are beyond the control of retailers.

3. Distribution – from “On-Shelf Availability” to “On Demand Availability”

Constantly under pressure to deliver merchandise according to their customers’ choice of place and time, has led retailers to rethink demand planning. Omni-channel and e-commerce have increased channel complexity and challenged existing fulfilment models.

The blurring of channel boundaries has led to an increasing number of permutations of fulfilment options expected by consumers, which changes order patterns and necessitates demand planning. Examples include:

- Multi-channel/omni-channel retail changes consumer order patterns. An example would be buying in-store and expecting home delivery or alternative site collection, then requesting free returns across all channels.

- Immediate fulfilment, such as same- or next-day delivery, is becoming the standard.

- Mobile shopping is increasingly bridging the gap between online and offline commerce.

- Returns policy/reverse logistics: Retailers need to plan for returns and exchanges, which account for 30% of e-commerce purchases, compared to just 8% for physical stores, according to CBRE. Data from MIT Sloan Management Review indicated that retailers spend $100 billion (3.8% of their profits) per year restocking and repackaging returns.

4. Increased Globalization – the Added Complexity of Sourcing from and Selling to Emerging Markets

On the supply side, retailers are increasingly sourcing from a wider range of partners in developing countries, in order to take advantage of the cost differentials in terms of labor and the raw materials of the various countries. For example, as costs in China have increased, there has been a shift in retailers’ sourcing needs – instead of solely relying on China, they now rely on a range of lower-cost countries. This increases the complexity of demand planning, as the other countries’ infrastructure may be less mature and more prone to negative externalities.

On the demand side, changes in global economics developments and demographics have given rise to the emergence of new consumer markets. Retailers with better retail-planning capabilities are best positioned to customize their offering to satisfy local consumer demands and seize the opportunity.

Existing Demand-Planning Processes are Inadequate

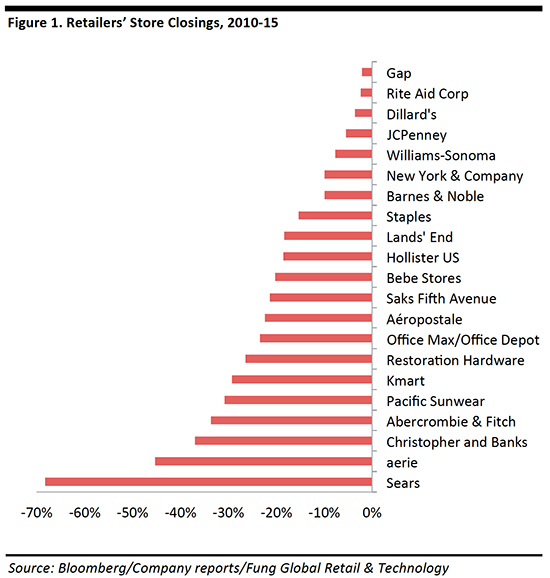

Many demand-planning processes and supply chains were built for supplying goods to physical stores, i.e. brick-and-mortar stores, and are now outdated and no longer able to meet the new norms of e-commerce and multi-channel retail. Hence, it is critical for retailers to improve their demand-planning capabilities in order to cope with the increasing demands from consumers.

A study on demand planning based on retailers’ self-assessment data found that some retailers’ demand planning lacks maturity and can be overwhelmed by unforeseen demand fluctuations. Some retailers are relatively new to establishing mature demand-planning processes.

THE CHALLENGES OF NEW CONSUMER NORMS TO DEMAND PLANNING

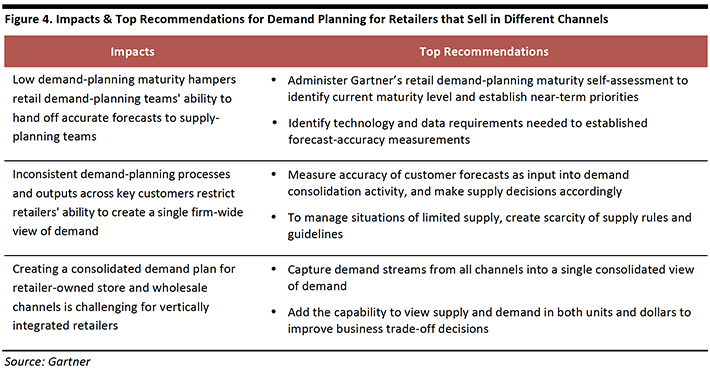

Retailers often find it challenging to match supply and demand across multiple customers and channels.

Challenges Amplified for Retailers that Sell Across Different Channels

The challenge for demand planning is exacerbated for retailers that have to match supply and demand across multiple channels (owned stores, wholesale, online and franchised stores). In addition to their direct-to-customer business, these retailers are exposed to the externalities of demand planning, as they typically depend on their wholesale and franchisee customers for consistent and trustworthy demand plans.

The bullwhip effect refers to increasing swings in demand order variability in the supply chain, which are amplified as one moves up the supply chain. An example would be due to the variability in wholesale orders: a distributor likely relies on external resellers’ demand forecasts to make their inventory forecasts. However, this exposes a distributor to order swings when resellers supply inferior order forecasts. Over time, some distributors have responded by paring down on their proportion of revenue from wholesale channels.

Nike: Nike launched its direct-to-customer (DTC) initiative, which focuses on direct selling to customers. The decline in wholesale channel sales is a general trend among apparel companies that are increasing their focus on the higher-margin retail channel where they have an opportunity to build their brand relationship with customers and collect customer data.

Under Armour: The revenue share of Under Armour’s wholesale segment has declined from 73% of total sales in FY2010 to 66% in the last fiscal year.

VF Corp: VF Corp.’s wholesale revenue as a percentage of total revenue has declined from 81% in FY2010 to 72% in the last fiscal year.

Other retailers have increased the amount of excessive inventory as a buffer against sharp fluctuations in demand.

It would benefit retailers to control the bullwhip effect and improve their supply-chain performance by coordinating information and demand planning.

OTHER KEY CHALLENGES IN THE AREA OF DEMAND PLANNING

We have identified other major challenges that retailers face in demand planning, which include:

- Insufficient internal collaboration leading to disaggregated demand forecast outputs: There may be a lack of communication and coordination among departments. This results in siloed demand planning across owned-stores, wholesale and e-commerce channels rather than a firm-wide forecast for demand.

- Poor data integrity: The lack of an integrated demand-planning tool or process will lead to inconsistent demand forecasts. For example, some retailers may still be relying on spreadsheets for forecasting.

- Lack of robust forecast assumptions and methodology: Irregular sales promotions and marketing activities that impact sales, but do not have historical patterns, may be left out of a demand-planning model that relies on historical patterns.

- Lack of standardization with resellers: The resellers and franchisees that retailers sell to may lack the technology standardization and formal sales and operations planning (S&OP) processes.

- Difficulty in getting timely customer demand data.

WHAT THE CHANGES MEAN FOR DEMAND PLANNING

The emerging norms of consumer demand will increasingly challenge companies’ demand-planning processes across multiple dimensions, such as merchandise planning, responsiveness to consumer demand and forecasting ability.

Introducing “Total Demand Forecasting”

Total demand forecasting refers to establishing a forecast for total global demand across multiple sales channels – owned-store, wholesale and e-commerce. A retailer will need to be able to plan, track and forecast total consumer demand in today’s world of chanel proliferation (stores, e-commerce, wholesale, international). Forecasts should be on an aggregate level, not the level of the individual item, to enable the retailer to plan for capacity and factor in events that might impact demand, such as new product launches, sales promotions and advertising campaigns.

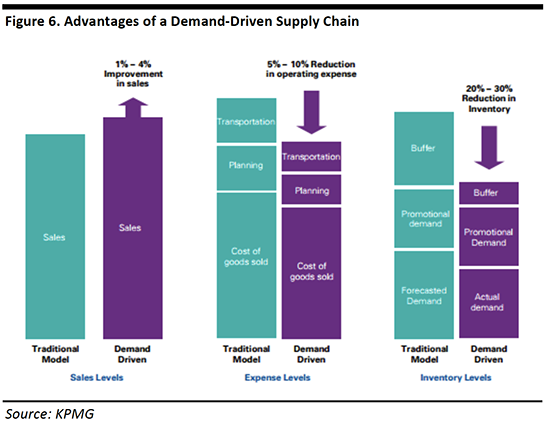

Introducing Demand Planning to the Demand-Driven Supply Chain (DDSC)

The focus has been for retailers to move from a forecast-driven mentality to a demand-driven one, as a more proactive stance to the demand-planning process. A demand-driven mentality is embodied in the concept of a demand-driven supply chain (DDSC) as opposed to the traditional forecast-led supply chains.

The Key Benefits of Demand Planning

The aim of demand planning is to ensure that a retailer can achieve the highest level of customer satisfaction through on-time deliveries with minimum inventory and costs.

The key business benefits that can be derived from demand planning solutions are:

- Accurate inventory levels forecasts across all channels and regions.

- Increased efficiencies and streamline processes.

- Improved customer satisfaction.

- Ability to respond to extreme seasonality and volumes, optimized inventory positions.

- Seamless integration across multiple channels.

1. Improved Financial Performance

Retailers with best-in-class demand-planning processes are better positioned to outperform their peer group on most operating and financial metrics. In general, companies with more sophisticated demand-planning processes have less inventory, higher asset utilization and shorter cash collection cycles than their peers, leading to major cost savings.

Surveys have also shown that demand-forecast accuracy leads directly to a higher return on assets and improved profit margins. Further benchmarking reports show that for every 1% improvement in forecast accuracy, companies report a 1-2% drop in inventory levels.

Introducing Inventory Turnover and Why It Matters for Retailers

The inventory turnover ratio measures how efficiently a company manages inventory, and the rate at which inventory is sold over a specific period. The inventory turnover ratio and profit margins are the primary drivers that directly impact return on capital (ROC), which measures how well a company uses its capital to generate returns. In general, a higher inventory turnover ratio is preferred, as it indicates that a retailer is efficient in turning its inventory to sales.

Advantages of high inventory turnover for a retailer:

- Better financing terms: Higher inventory turnover allows a retailer to rely on its suppliers’ capital to finance its inventory rather than its own capital. When inventory is turned over more rapidly, more inventories are financed through payment terms provided by suppliers rather than a retailer’s working capital.

- Lower risk of obsolescence: A higher inventory turnover serves as a moat for retailers’ profit margins. Should a retailer’s rate of inventory turnover dip, there is the risk of the inventory turning obsolete, or the risk of having to liquidate inventory at suboptimal prices.

- Higher operating leverage: Higher inventory turns means that operating costs can be spread across a larger revenue base. Retailers will be able to charge lower prices relative to their peers, which sets off a virtuous cycle of lower prices attracting customers to shop at their stores.

More sophisticated demand-planning solutions seek to address the underlying reasons that could lead to a low inventory turnover ratio, which include a retailer:

- Making inefficient inventory purchasing decisions.

- Keeping too much inventory on hand. Retailers that have excessive inventory on hand may need to sell off their obsolete inventory at heavily discounted prices, which depresses profit margins.

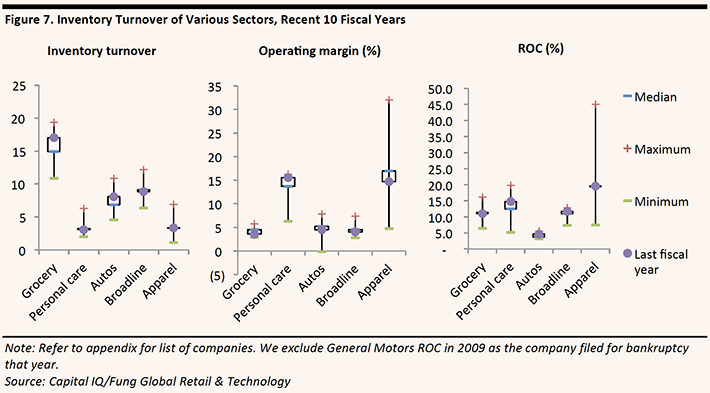

FINANCIAL ANALYSIS OF INVENTORY TURNOVER

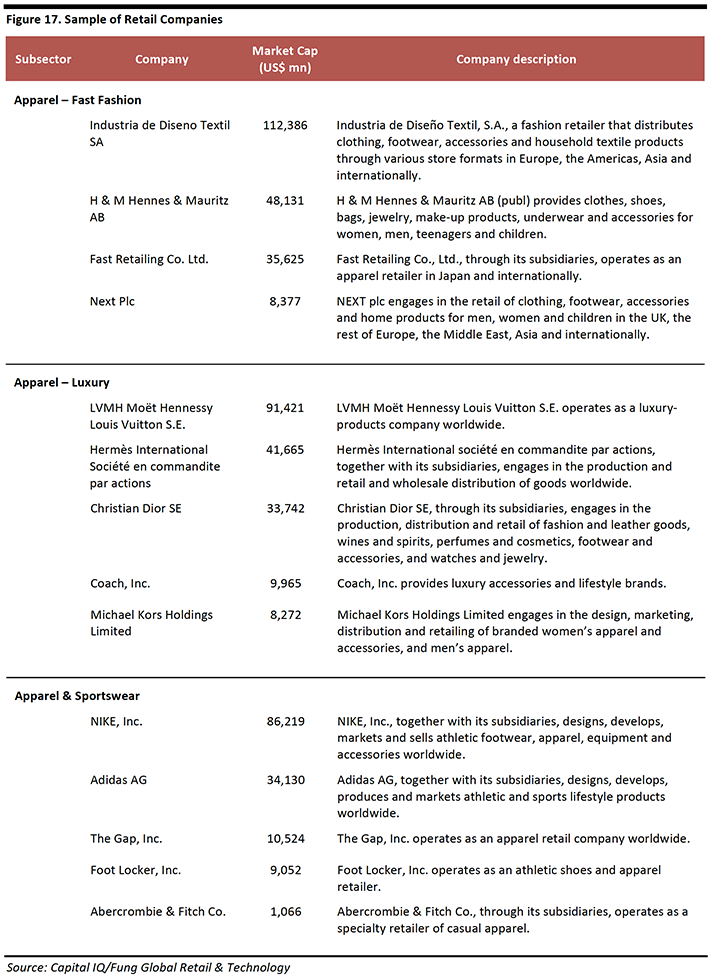

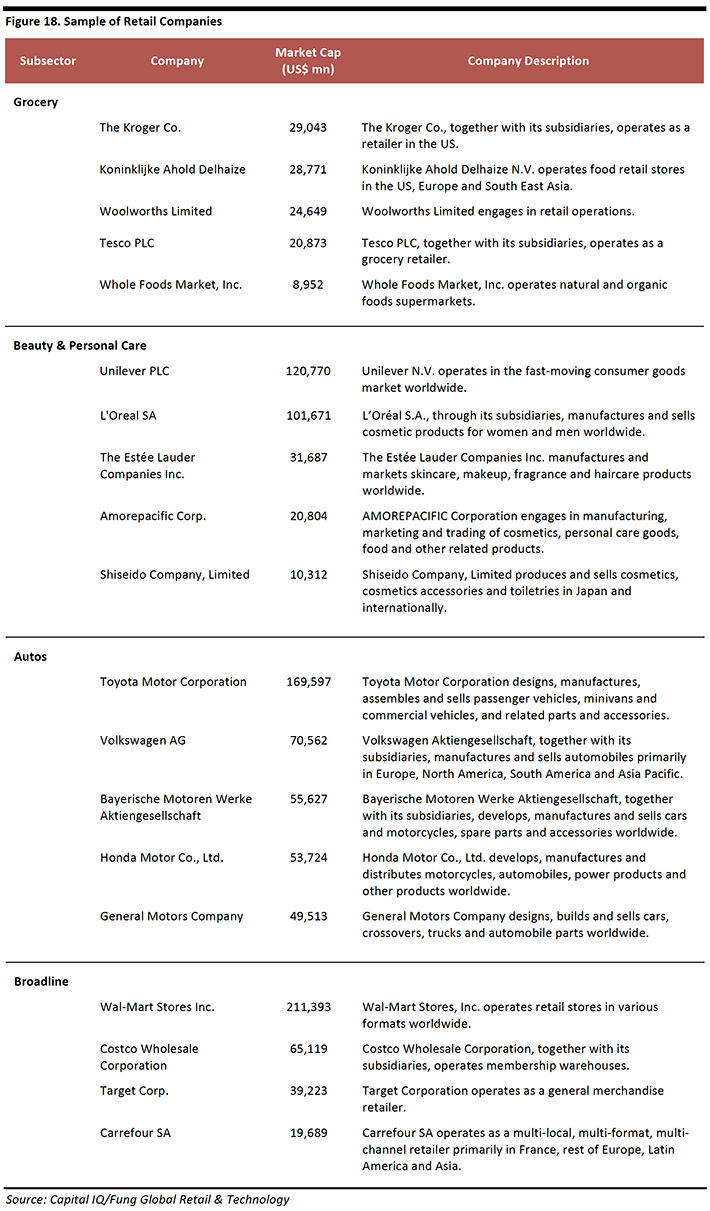

Below, we compare selected retailers’ inventory turnover ratios and operating margin, the two components of return on capital (ROC). Our sample includes a total of 33 leading retailers globally. Please refer to the appendix for details.

We compare the inventory turnover ratios of similar retail companies, with the idea that it might not be a good indicator of company performance of retailers with different business models. Inventory turnover is defined as the amount of inventory sold, divided by the average inventory during the period.

Key takeaways

Inventory turnover

- The inventory turnover ratios for grocery and autos in the last fiscal year were above the recent 10-year median.

- One concern: The inventory turnover ratio of broadline was below the 10-year median, while that of apparel was broadly in line, indicating an urgent need for improvement through better demand-planning processes.

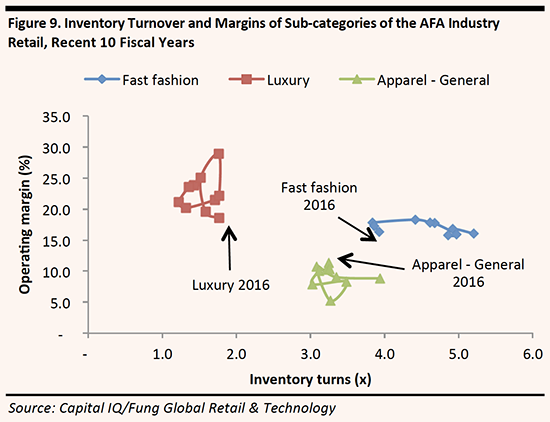

Apparel

- Most volatile margins and returns: Apparel has the most volatile operating margins and ROC, reflecting the challenging apparel landscape that is defined by declining mall traffic and fierce competition. Given that inventory turns is a metric that is more controllable by apparel retailers, we believe better demand planning is one of the best ways for retailers to improve their financial performance.

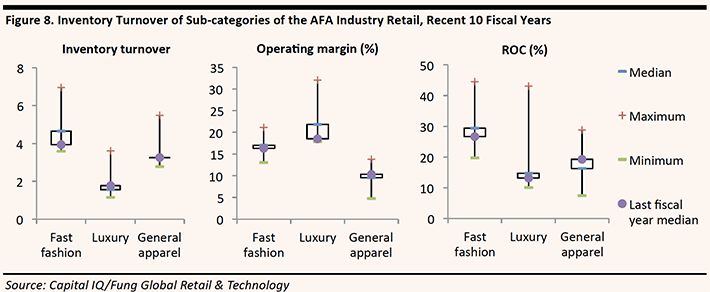

Apparel – Measuring the Performance of Subcategories

- The relatively wide range between the historical maximum and minimum inventory turnover ratio imply that there is much room for improvement through better demand planning.

- The inventory turnover ratios of fast-fashion and general apparel in the most recent fiscal year are below the historical 10-year median.

Conclusions

Retailers with the highest inventory turnover include grocery and fast fashion, industries defined by relatively higher volumes. High inventory turnover in low-margin industries is necessary to offset lower per-unit profits with higher unit sales volume and remain cash-flow positive.

2. The Impact of Distributing on Different Channels

We also examine the impact of shifting distribution models to demand planning needs. The three ongoing trends that have been impacting the distribution model and profitability of brands and retailers are:

- The increasing prominence of e-commerce.

- The scaling back of retailers from wholesale distribution.

- The omni-channel strategies of retailers.

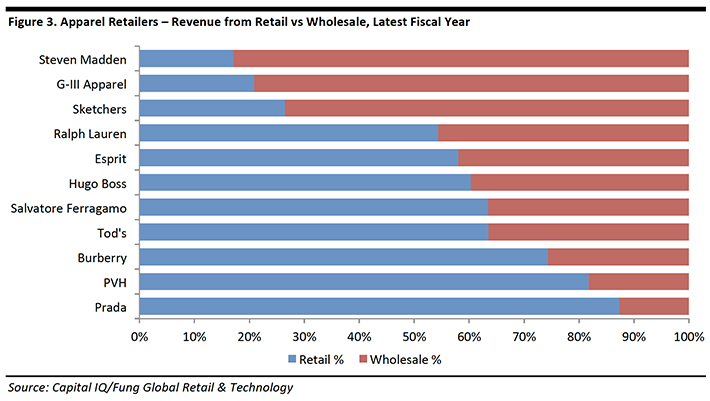

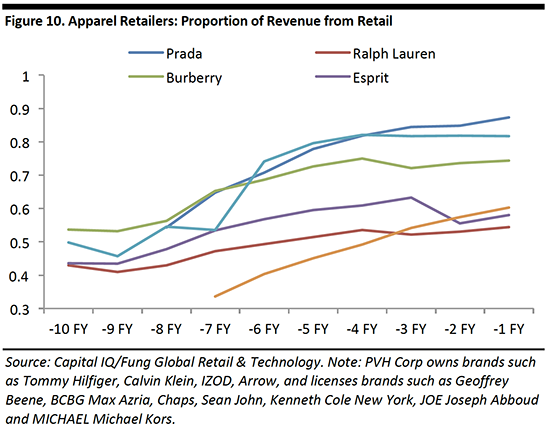

Brands Leaning Towards Omni-Channel and DTC Strategies

Some apparel retailers such as Nike, VF Corp and G-III Apparel Group are scaling back their wholesale operations and focusing more on DTC (direct to customer) channels, resulting in increasing DTC contribution to the sales mix. For other brands, such as Sketchers and Burberry, their most recent financial results were negatively impacted by wholesale distribution.

The Problem for the Wholesale Distribution Model

Wholesale distribution suffers from the shortcomings and negative externality in predicting wholesale demand with accuracy, which is one reason driving a trend for retailers to shift from a wholesale to a retail distribution model.

For example, resellers who buy from these brands may have less sophisticated demand-planning systems that cause them to place orders based on inaccurate demand forecasts. These resellers may cancel and return orders or sell products at heavily discounted prices. Selling at a lower ASP would lead to lower profitability.

Generally, DTC revenue earns higher margins for apparel companies compared to sales through the wholesale channel. However, we believe the wholesale revenue model is here to stay.

3. Demand Planning Processes are Increasingly Embedded into an Organizational Culture

Demand planning plays a critical role in helping retailers achieve their growth objectives, as it is an integrated business-planning process that drives decision making at the enterprise level.

Demand planning should capture the total global demand across all sales channels, which serves as a foundation for stakeholders of a company to plan ahead. The data is available for, and can be used to support, other functional areas in making operational and managerial decisions.

Better demand-planning solutions lead to more consistent demand forecasts, which enable retailers to create a single, firm-wide view of demand.

As demand planning is closely tied with overall profitability and the health of a retailer, below are some notable trends in the area:

- Increasing frequency of sales and operations planning: Historically, demand and capacity planning was done in monthly cycles. Nowadays, many companies have sped up their planning cycles to weekly, or as often as daily for fast-moving categories.

- Demand planning established as a best practice: The breadth of demand planning can be broadened to cover Integrated Business Planning (IBP), which allows stakeholders to be involved in balancing supply and demand in a way that maximizes profits.

- Companies can integrate the value of their products into demand planning: Instead of merely reacting to market changes, organizations can proactively shape their demand. For example, a retailer can decide to shift demand to higher-margin products.

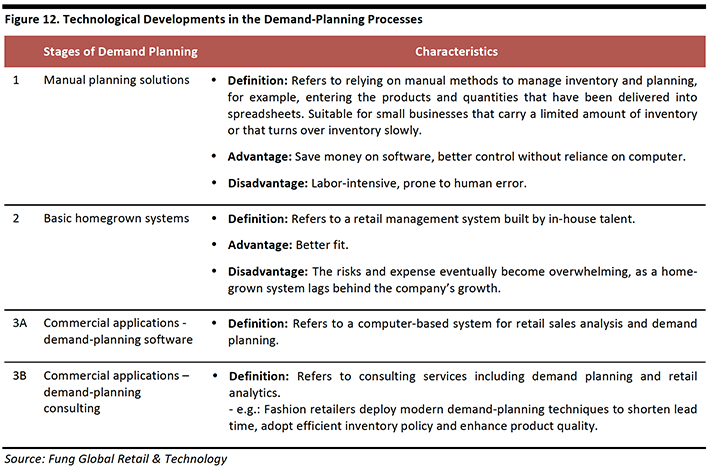

Technological Developments in Demand Planning Solutions

The demand-planning process has evolved over time to incorporate more integrated processes and better capture an enterprise view of demand.

For example, mature demand-planning solutions make use of predictive analytics to establish accurate demand forecasts that can be readily applied to total consumer demand forecasting.

Below are some benefits and unique functions of proprietary demand-planning solutions:

- Provide enterprise level visibility into demand across all distribution channels and regions.

- Offer a clear methodology and implementation strategy to optimize planning and forecasting.

- Demonstrate the exact relationship between product and profits.

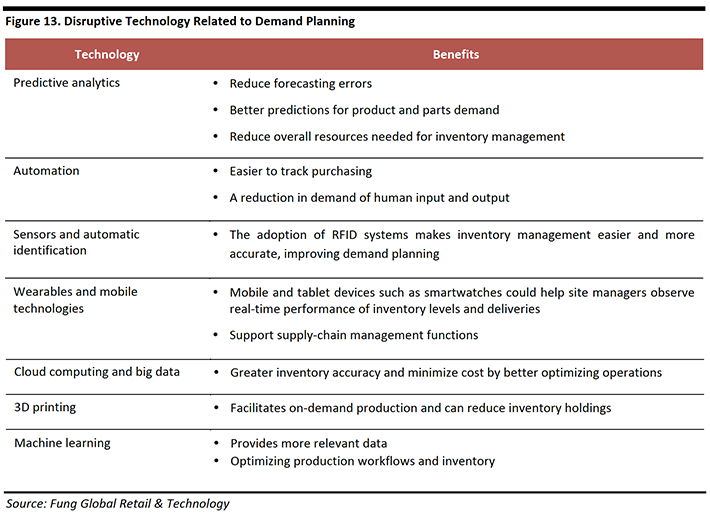

Evolution and Future State of Demand Planning

We highlight other technologies that can facilitate or potentially disrupt demand planning in the following table.

COMMERCIAL APPLICATIONS OF DEMAND PLANNING

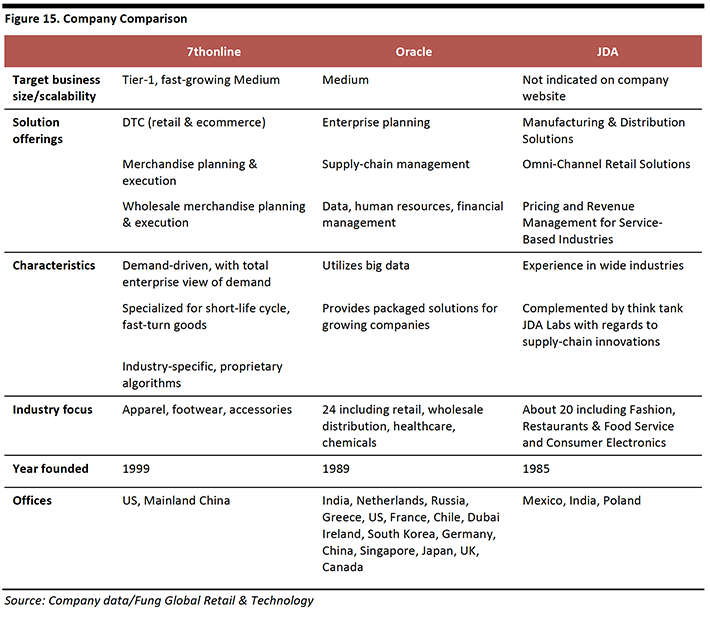

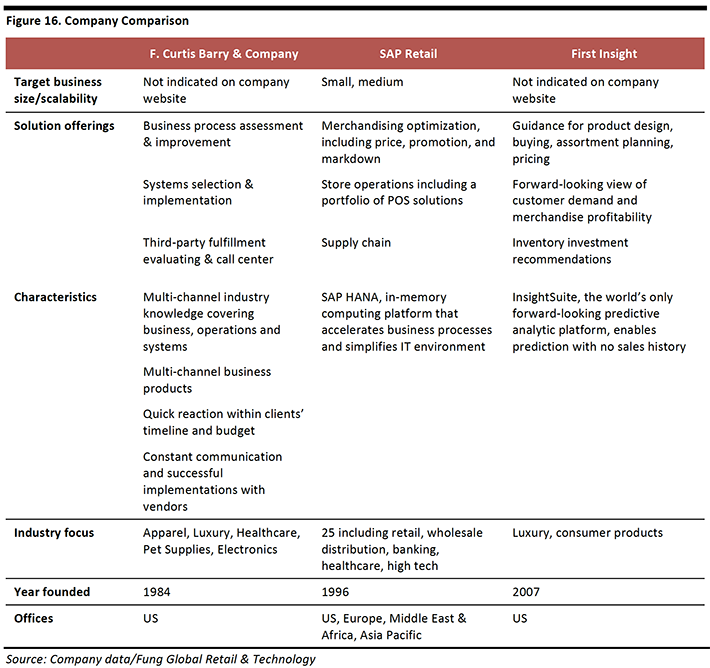

Commercial applications that provide tools and advice for retailers for demand planning include the following (Refer to the appendix for details on the demand-planning solutions for selected peer groups.).

- 7thonline

- Curtis Barry & Company

- Oracle

- JDA

- SAP Retail

- First Insight

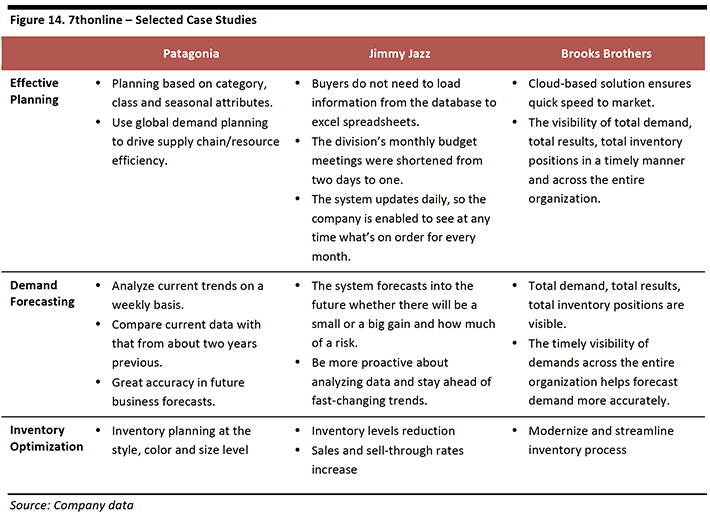

INTRODUCING 7THONLINE

7thonline is a company that provides cross-channel, global demand planning solutions for the Apparel, Footwear, and Accessories (AFA) industry. 7thonline offers cloud-based solutions that are specifically designed for the AFA industry covering all channels, including wholesale, retail and ecommerce. The company provides a basis for planning global demand, rather than being limited by a retail-heavy worldview.

Distinguishing Features of 7thonline

- Provides both retail-/store-based and wholesale-/account-based assortment planning.

- Provides corporate-level demand-planning services for corporate teams to see total demand, followed by planning, forecasting and tracking.

- Possesses AFA industry-specific knowledge, specialized for short-life cycle and fast-turnover goods.

- Advanced cloud-based technologies such as AFA industry-specific and proprietary algorithms.

The key capabilities of 7thonline span planning, demand forecasting and inventory optimizing for omni-channel brands, including:

- Provides a comprehensive assortment and size optimization service that adopts its technologies, such as proprietary optimization algorithms.

- Provides customers with real-time inventory information with its cloud-based technologies.

- Provides consulting services, as well as ensures efficient implementation with quick outcomes.

- Provides comprehensive services covering planning, demand forecasting and inventory optimization for omni-channel brands.

How 7thonline Works

7thonline has built out tools to support these types of complex multichannel brands. These brands can use 7thonline to perform both retail-/store-based planning and wholesale-/account-based assortment planning.

- 7thonline gets to know clients’ needs according to their selection of planning plans.

- For better merchandise and assortment planning services, 7thonline analyzes the clients’ performance or indicators, and provides an optimized plan for clients.

- Details such as inventory and sales information will be updated in the system with accuracy and speed.

- 7thonline enables clients to forecast and make reports.

According to users, the benefits of 7thonline include improved sales, profitability and more efficient working capital management. For example, the overall results for a direct-to-consumer suite saw up to 30% lower markdowns, a 5-10% increase in full-price sell-through, a 1-3% reduction in lost sales, 1-3 times greater inventory turns and up to a 30% reduction in administrative expenditures, according to the company’s official site.

APPENDIX